- Have Questions? Talk to Us

- info@procizo.com

What Is Underwriting? Complete Guide for Business Lending (2026)

The Complete Guide to MCA Underwriting Outsourcing (2026)

June 9, 2026What Is MCA Underwriting? The Complete Process for Funders (2026)

June 9, 2026

Table of Contents

- underwriting-kpo/ target=_blank rel=noopener noreferrer>underwriting>What Is Underwriting?

- What Is an Underwriter?

- Underwriting in Finance: Types

- Loan Underwriting Process

- MCA Underwriting: Key Differences

- lending-underwriting>What Funders Check

- Underwriting in Business Development

- Underwriting vs. Approval

- FAQ

| Key Takeaways

Underwriting definition: The risk evaluation process financial institutions use before lending money or extending credit. What an underwriter does: Reviews applications, verifies financial documents, assesses risk, and decides – approve, decline, or modify terms. Why MCA underwriting is different: Focuses on daily revenue consistency, ACH payment history, holdback capacity, and stacking risk – not credit scores or collateral. Why it matters: Without underwriting, lenders have no systematic way to price risk, detect fraud, or maintain portfolio performance. Procizo Outsourcing LLC provides outsourced MCA underwriting services to US-based funders and brokers, processing standard files in under 24 hours. |

– Content Writer, Procizo Outsourcing LLC. All content reviewed by the Procizo Operations Team with 5+ years of combined MCA underwriting experience servicing US-based funders and ISO partners.

About Procizo Outsourcing LLC: Specialized MCA underwriting and back-office support provider. Our team processes bank statement scrubbing, paper grading, and funding decisions for funders handling 30-100+ deals per month.

1. What Is Underwriting? Definition & Meaning

Underwriting is the systematic process of evaluating financial risk before capital changes hands. The term originates from the historical practice where risk-takers would write their names under the total amount of risk they agreed to cover – literally “writing under the risk [R1].

In modern finance, underwriting answers a single critical question: What is the likelihood that this borrower will default? The underwriter evaluates financial data – revenue, credit history, bank statements, debt obligations, and industry risk – to assign a risk grade and determine funding terms.

What does underwriting mean for business owners? When a business applies for funding, underwriting is the stage where the lender verifies everything. It’s not a rubber stamp – it’s the most important step in the lending process because it separates data-driven decisions from guesswork.

2. What Is an Underwriter? Role & Responsibilities

What is a underwriter? An underwriter is a trained financial professional who evaluates risk and makes funding decisions on behalf of a lender. The term “underwriter comes from the historical practice where individuals would write their names under the total risk they agreed to cover. An underwriter is the financial professional who evaluates risk and makes funding decisions on behalf of a lender, insurer, or investment firm. In business lending, underwriters review loan and MCA applications, analyze financial documents, and decide whether to approve, decline, or modify terms [R2].

What Does an Underwriter Do Daily?

- Review funding applications – Check for completeness, red flags, and documentation quality

- Analyze bank statements – Calculate average daily balances, flag NSF items, identify revenue trends

- Verify financial documents – Authenticate tax returns, bank statements, and business licenses

- Assess credit profiles – Evaluate personal and business credit scores, payment history, outstanding debt

- Assign risk grades – Classify applications A through D based on risk level

- Make funding decisions – Approve, decline, or set conditions for approval

- Communicate with brokers – Clarify discrepancies and request additional documentation

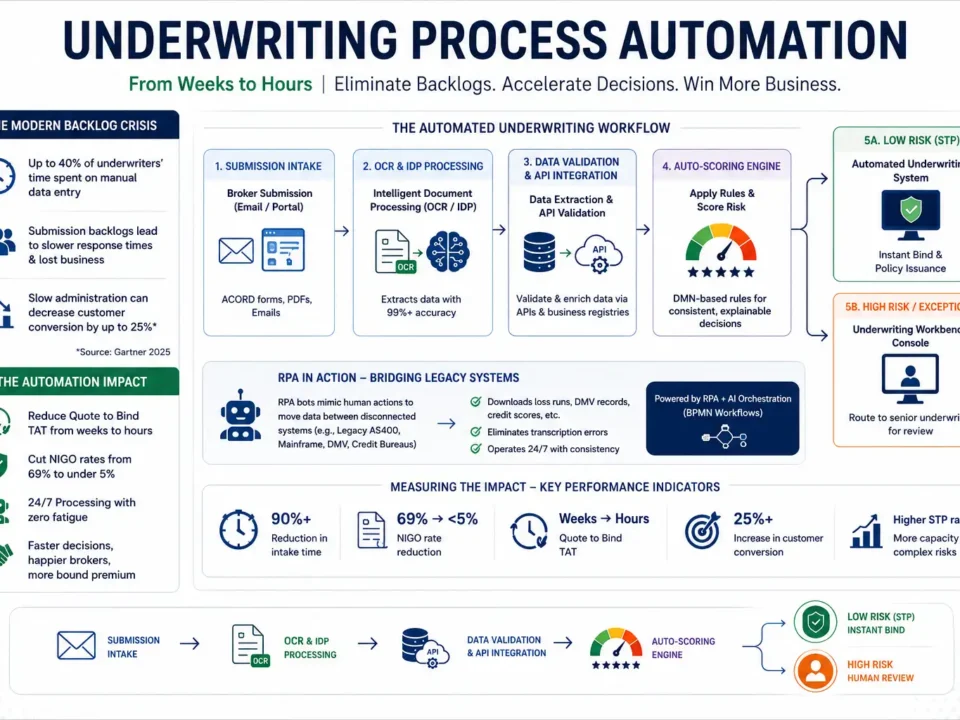

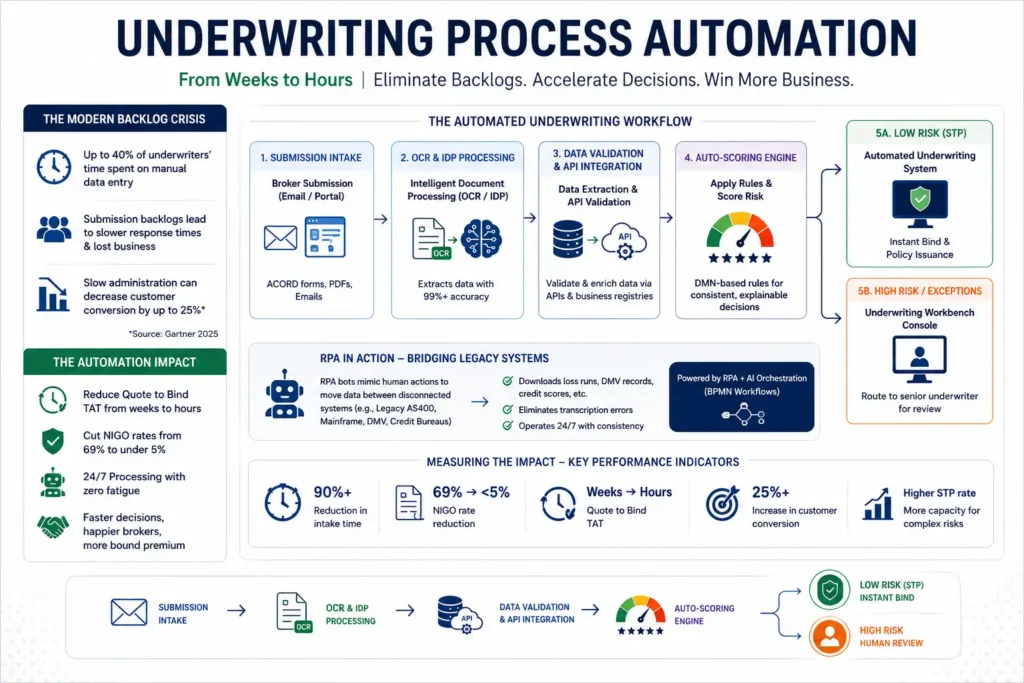

What do underwriters do all day? In MCA lending, underwriters spend most of their time scrubbing bank statements – extracting deposit data, flagging negatives, and calculating true revenue. A single file can take 2-4 hours to underwrite manually, which is why many funders outsource this function.

Related: Loan Underwriting Process: Complete Guide for Lenders (2026) | Merchant Cash Advance: The Complete Guide for Borrowers and Lenders (2026) | MCA Underwriting: The Complete Guide to Merchant Cash Advance Underwriting Process

3. What Is Underwriting in Finance? Types Compared

Underwriting exists in several forms across finance. Each type evaluates different risks [R1]:

| Type | What It Evaluates | Decision Time | Example |

|---|---|---|---|

| Loan/Business Underwriting | Cash flow, revenue, credit, debt capacity | 24 hours – 5 days | MCA advance, SBA loan, term loan |

| Mortgage Underwriting | Property value, personal income, DTI, credit score | 30 – 60 days | Home purchase, refinance |

| Insurance Underwriting | Lifestyle, health, property condition | Days – weeks | Life, health, auto insurance |

| Securities Underwriting | Company valuation, market demand, regulation | Months | IPOs, bond offerings |

The key difference for MCA and alternative lending is speed and data focus. Business lending underwriting must be faster than mortgage underwriting and relies more on real-time cash flow data than on long-term credit history.

What Is Underwriting in Business Development?

Underwriting in business development refers to how underwriters and BD teams collaborate to assess deals quickly. In MCA lending, BD brings in applications and pre-qualifies leads based on basic criteria. Underwriting then verifies data and makes the final decision. The closer these teams work, the faster deals fund and the more deals close per month. This is why many growing funders outsource underwriting – to eliminate the bottleneck between sales and funding [R3].

4. What Is the Underwriting Process? A Step-by-Step Guide

What is loan underwriting? Loan underwriting is the systematic evaluation of a borrower’s ability to repay a loan. It involves analyzing financial data, verifying documentation, and determining risk before approving or declining a funding request. Loan underwriting is the evaluation of a borrower’s ability to repay a loan. What is the underwriting process? The underwriting process follows a structured flow from application to funding decision. Each step moves the file closer to a final approval or decline decision, and each step requires different analysis and verification. The underwriter reviews financial data, verifies documentation, and determines risk before the loan is approved [R4].

What is underwriting a loan step by step?

- Application intake – Broker submits the application package with basic information and documents

- Document collection – Bank statements (3-6 months), business license, ID, voided check, tax returns

- Financial analysis – Underwriter scrubs bank statements: extracts deposits, flags NSF items, calculates daily balances and true revenue

- Risk assessment – Evaluates data against lending criteria: revenue thresholds, time in business, credit scores, existing debt

- Paper grading – Assigns risk grade (A through D). A-paper = lowest risk, D-paper = highest risk

- Pricing – Sets factor rate, advance amount, and holdback percentage based on risk grade

- Decision – Approval (with or without conditions), decline, or request for more information

In MCA underwriting, the process is compressed. A standard file can go from application to decision in under 24 hours when handled by an experienced underwriting team – compared to 30-60 days for mortgage underwriting.

Automated vs. Manual Underwriting

Modern underwriting operations use two approaches. Automated underwriting relies on algorithms and predefined rules to evaluate applications – checking revenue thresholds, credit scores, and basic eligibility in seconds. Many online lenders and fintech platforms use automated underwriting for initial screening. Manual underwriting involves a human underwriter who reviews the complete file, interprets nuanced financial data, and makes judgment calls that algorithms cannot replicate. Manual underwriting is essential for MCA deals where bank statements show irregular deposits, seasonal patterns, or borderline credit profiles that require expert analysis. Most professional MCA underwriting operations use a hybrid approach: automated pre-screening for obvious approvals and declines, followed by manual review of the remaining files [R4].

Loan Underwriting vs. MCA Underwriting – Side by Side

| Factor | Traditional Loan Underwriting | MCA Underwriting |

|---|---|---|

| Primary data source | Tax returns, credit score | Bank statements, processing data |

| Repayment structure | Fixed monthly payments | Daily ACH percentage of sales |

| Credit score weight | High (primary factor) | Moderate (secondary to cash flow) |

| Typical turnaround | 3-30 days | 24 hours – 5 days |

| Key risk indicators | DTI ratio, collateral value | NSF items, stacking, daily balance |

| Collateral requirement | Usually required | Unsecured (personal guarantee) |

5. MCA Underwriting – What Makes It Different

MCA (Merchant Cash Advance) underwriting is fundamentally different from traditional loan underwriting. It evaluates a merchant’s ability to repay through daily ACH payments tied to their revenue, not through fixed monthly installments [R3].

Five factors that set MCA underwriting apart:

- Daily cash flow focus – Underwriters analyze daily bank deposits, not monthly revenue. Consistency across 90-180 days matters more than total annual revenue

- Holdback percentages – The underwriter determines the right daily repayment percentage (typically 8-15%) based on revenue and risk grade

- NSF analysis – Non-sufficient funds occurrences are the strongest predictor of default. More than 3 NSF items in 90 days typically downgrades the paper grade

- Stacking risk – Underwriters check UCC filings to identify outstanding advances from other funders. Multiple active positions increase default risk significantly

- Paper grades – A-paper brings low factor rates (1.10-1.18) and low holdbacks (8-10%). D-paper carries factor rates of 1.30+ and holdbacks of 13-15%

This is why bank statement scrubbing is the most critical (and most time-intensive) part of MCA underwriting. The accuracy of deposit extraction, NSF identification, and revenue calculation directly determines portfolio performance. According to Nav.com, MCA underwriting evaluates recent business performance more heavily than traditional lending – focusing on the last 3-6 months of bank data rather than multi-year credit history [R3]. A clean underwriting process can mean the difference between a 5% default rate and a 15% default rate for the same portfolio of merchants.

Paper Grades Explained: How Underwriters Classify Risk

Paper grading is the backbone of MCA underwriting decisions. Each grade reflects a specific risk level and determines the terms a merchant can access.

Quick Reference: Paper Grades in MCA Underwriting

Source: Nav.com MCA Underwriting Guide [R3] |

Paper grading is the backbone of MCA underwriting decisions. Each grade reflects a specific risk level and determines the terms a merchant can access:

- A-Paper: Strong daily balances ($5,000+), minimal NSF occurrences, 12+ months stable revenue. Qualifies for lowest factor rates (1.10-1.18) and highest advance amounts with holdbacks of 8-10%

- B-Paper: Good revenue consistency, occasional NSF items, 6+ months in business. Factor rates of 1.18-1.25 with 10-12% holdback

- C-Paper: Moderate revenue, several NSF occurrences, some revenue volatility. Factor rates of 1.25-1.30 with 12-13% holdback

- D-Paper: Multiple NSF items, inconsistent deposits, possible stacking history. Factor rates of 1.30-1.40+ with 13-15% holdback, lower advance amounts [R3]

The difference between an A-paper and D-paper approval can mean thousands of dollars in effective interest cost for the merchant and significantly different portfolio risk for the funder. Accurate paper grading is the underwriter’s most important responsibility.

Bank Statement Scrubbing – The Technical Core

Bank statement scrubbing is the process of extracting and analyzing every transaction from a merchant’s bank statements. The underwriter identifies all deposits (filtering out transfers and non-revenue items), flags NSF occurrences, identifies negative daily balances, and calculates true revenue and average daily balances. A skilled underwriter can identify patterns that indicate undisclosed debt, revenue manipulation, or early warning signs of default. This process typically takes 2-4 hours per file when done manually – and it is the primary reason many funders outsource underwriting to specialized providers who have efficient systems and trained teams to handle it at scale [R5].

NSF, UCC Filings, and Stacking Risk

| Red Flag Alert: NSF Occurrences

More than 3 NSF items in 90 days = downgrade at least 1 paper grade. NSF analysis is one of the strongest predictors of default in MCA lending. Source: Nav.com [R3], industry underwriting standards |

NSF (non-sufficient funds) occurrences are among the strongest predictors of default in MCA underwriting. A merchant with more than 3 NSF items in the last 90 days is typically downgraded at least one paper grade. Underwriters also check UCC (Uniform Commercial Code) filings to identify outstanding advances from other funders – this reveals stacking risk, where a merchant has taken advances from multiple funders simultaneously without disclosing all positions. Stacked merchants have significantly higher default rates because their total daily repayment obligations across all positions can exceed their daily cash flow capacity [R4]. A thorough underwriter calculates the merchant’s total daily payment obligations across all positions and compares it to their average daily balance to determine if the cumulative holdback is sustainable.

6. Business Lending Underwriting – What Funders Actually Check

When evaluating a business for a loan or advance, underwriters focus on five key areas [R4]:

- Bank statements: 3-6 months of business bank accounts to verify revenue, detect NSF items, calculate average daily balances, and identify undisclosed debt

- Credit history: Personal and business credit scores, payment patterns, outstanding obligations. In MCA, credit is secondary to cash flow but still affects terms

- Revenue consistency: Monthly revenue trends, seasonal fluctuations, deposit patterns. Steady $40K/month is better than volatile $80K/month

- Debt load: Existing advances, loan payments, total daily repayment obligations. High debt-to-revenue ratios reduce available capacity

- Industry risk: Business type, time in operation, failure rates by sector. Restaurants, construction, and seasonal retail face stricter criteria

Each factor contributes to the paper grade. A B-paper merchant with $30K average monthly deposits, 2 years in business, and 660 FICO might qualify for a $25K advance at 1.22 factor rate with 10% holdback. The same candidate rated C-paper might only get $18K at 1.32 with 13% holdback. The quality of underwriting directly determines access to capital.

Common Underwriting Challenges for Funders

MCA funders face several operational bottlenecks that limit deal flow and portfolio performance:

- Scaling problems: One underwriter can process 3-5 deals per day. Growing beyond 30 deals per month requires larger teams that take weeks to hire and months to train

- Data verification complexity: Manual bank statement scrubbing is error-prone and time-consuming. Each file requires meticulous attention to detail that is difficult to maintain at scale

- Consistency across underwriters: Different underwriters may apply different standards to similar files, leading to inconsistent paper grading and unpredictable portfolio performance

- Turnaround time pressure: In a competitive market, the funder who delivers a decision first often wins the deal – but speed cannot come at the cost of accuracy

These challenges are why outsourcing underwriting has become a strategic move for growing MCA funders. It provides flexible capacity, standardized processes, and faster turnaround without the overhead of building an in-house team from scratch.

7. Underwriting in Business Development – Speed Wins Deals

In the MCA industry, multiple funders often evaluate the same merchant. The funder that delivers a decision first usually wins the deal. This makes underwriting speed a competitive advantage, not just an operational metric [R5].

Each in-house underwriter adds $65,000-$85,000 in annual salary plus 4-8 weeks of ramp-up time before reaching full productivity. For companies processing 30-100+ deals per month, building an in-house team becomes expensive and slow to scale.

This is why a growing number of MCA funders partner with specialized underwriting outsourcing providers. Outsourcing gives funders access to trained underwriters who process files in under 24 hours, with documented accuracy rates, without the fixed cost of full-time employees.

8. Underwriting vs. Approval – Not the Same Thing

A common misunderstanding is confusing underwriting with approval. They are related but distinct [R1]:

- Pre-qualification: Self-reported information – not verified, not guaranteed

- Application submitted: File enters the underwriting queue

- Underwriting: Verification and risk analysis happen here – documents are tested for accuracy

- Conditional approval: Underwriter approves subject to conditions (additional documents, clarification)

- Final approval: All conditions met – file is ready for funding

- Funding: Money disbursed to the borrower

A file can go through underwriting and be approved, declined, or approved with modified terms. Underwriting is the evaluation process. Approval is the outcome.

9.

Case Study: Insurance Carrier – Policy Administration Outsourcing

Challenge: A mid-size P&C carrier issuing 80,000+ policies annually was struggling with policy administration backlogs. New business processing averaged 6 days, endorsement turnaround was 3 days, and renewal backlog during peak season required costly overtime and temp staffing.

Solution: Procizo Outsourcing LLC deployed a dedicated team of 8 policy administrators handling new business processing, endorsements, renewals, and certificate issuance – integrated directly with the carrier’s Guidewire PolicyCenter system via secure VPN.

Results (12 months):

- Cost per policy reduced from $28 to $10 – 64% savings

- New business turnaround reduced from 6 days to 28 hours

- Endorsement turnaround reduced from 3 days to 14 hours

- Peak season backlog eliminated – 100% on-time processing

- Administrative capacity expanded from 12 to 24 FTE-equivalent at lower total cost

- Quality score: 98.8% accuracy vs 95% in-house baseline

Challenge: A mid-size P&C carrier issuing 80,000+ policies annually was struggling with policy administration backlogs. New business processing averaged 6 days, endorsement turnaround was 3 days, and renewal backlog during peak season required costly overtime and temp staffing.

Solution: Procizo Outsourcing LLC deployed a dedicated team of 8 policy administrators handling new business processing, endorsements, renewals, and certificate issuance – integrated directly with the carrier’s Guidewire PolicyCenter system via secure VPN.

Results (12 months):

- Cost per policy reduced from $28 to $10 – 64% savings

- New business turnaround reduced from 6 days to 28 hours

- Endorsement turnaround reduced from 3 days to 14 hours

- Peak season backlog eliminated – 100% on-time processing

- Administrative capacity expanded from 12 to 24 FTE-equivalent at lower total cost

- Quality score: 98.8% accuracy vs 95% in-house baseline

Frequently Asked Questions

What does an underwriter do in simple terms? An underwriter reviews financial documents to decide whether to approve funding and determines the terms based on the level of risk they identify.

What is underwriting in simple terms? Underwriting is the process of evaluating risk before lending money. It answers: “How likely is this borrower to pay us back?

What does underwrite mean? What is to underwrite? To underwrite a loan, policy, or deal means to evaluate the risk and accept financial responsibility for it. This is the active verb form – the action taken by an underwriter. When a funder asks “should we underwrite this deal?, they are asking whether to commit capital based on risk analysis. To underwrite means to accept financial responsibility for a loan, policy, or investment after evaluating the associated risk.

What do underwriters do all day? Underwriters review applications, analyze financial documents, calculate risk scores, make funding decisions, and communicate with brokers to clarify issues.

How is MCA underwriting different from traditional loan underwriting? MCA underwriting focuses on daily revenue, holdback percentages, and stacking risk rather than credit scores, DTI ratios, and collateral.

What is underwriting in business development? Underwriting in business development refers to how underwriters and sales teams collaborate to assess deals quickly and move them from application to funding.

What does the underwriting process involve? The process involves document collection, financial analysis, risk assessment, paper grading, pricing, and the final funding decision.

What are paper grades in MCA underwriting? Paper grades (A through D) classify risk level. A-paper is lowest risk with best terms. D-paper is highest risk with higher factor rates and holdbacks.

10. Ready to Streamline Your Underwriting?

Procizo provides outsourced MCA underwriting, bank statement scrubbing, and back-office support for US-based funders and brokers. Our teams process standard files in under 24 hours with documented accuracy. Contact us to start with a free pilot – send us your first 5 files and see the difference in turnaround time and accuracy before committing to a long-term partnership.

References

| Code | Source | Link |

|---|---|---|

| [R1] | IBISWorld – Industry Research & Market Data | View ? |

| [R2] | Dun & Bradstreet – Industry Research & Market Data | View ? |

| [R3] | Experian – Industry Research & Market Data | View ? |

| [R4] | Federal Reserve – Industry Research & Market Data | View ? |

| [R5] | SBA – Industry Research & Market Data | View ? |

| [R6] | Procizo Outsourcing LLC – Loan Underwriting Process: Complete Guide for Lenders (2026) | View ? |

| [R7] | Procizo Outsourcing LLC – Merchant Cash Advance: The Complete Guide for Borrowers and Lenders (2026) | View ? |

| [R8] | Procizo Outsourcing LLC – MCA Underwriting: The Complete Guide to Merchant Cash Advance Underwriting Process | View ? |

| [R9] | Procizo Outsourcing LLC – What Is MCA Underwriting? The Complete Process for Funders (2026) | View ? |

| [R10] | Procizo Outsourcing LLC – The Complete Guide to MCA Underwriting Outsourcing (2026) | View ? |

| [R11] | Procizo Outsourcing LLC – Lending Business: The Ultimate Playbook for Starting & Scaling | View ? |

Ready to Streamline Your Underwriting Support?

Procizo Outsourcing LLC provides end-to-end underwriting support with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement – no long-term commitment required.

No commitment required . 2-3 week onboarding . SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}

{kind=link}