- Have Questions? Talk to Us

- info@procizo.com

Life & Health Underwriting Operations: Outsourcing for Speed & Scale

On-Demand Underwriting Capacity: Scale Insurance Operations

May 20, 2026

The Complete Guide to MCA Underwriting Outsourcing (2026)

June 9, 2026

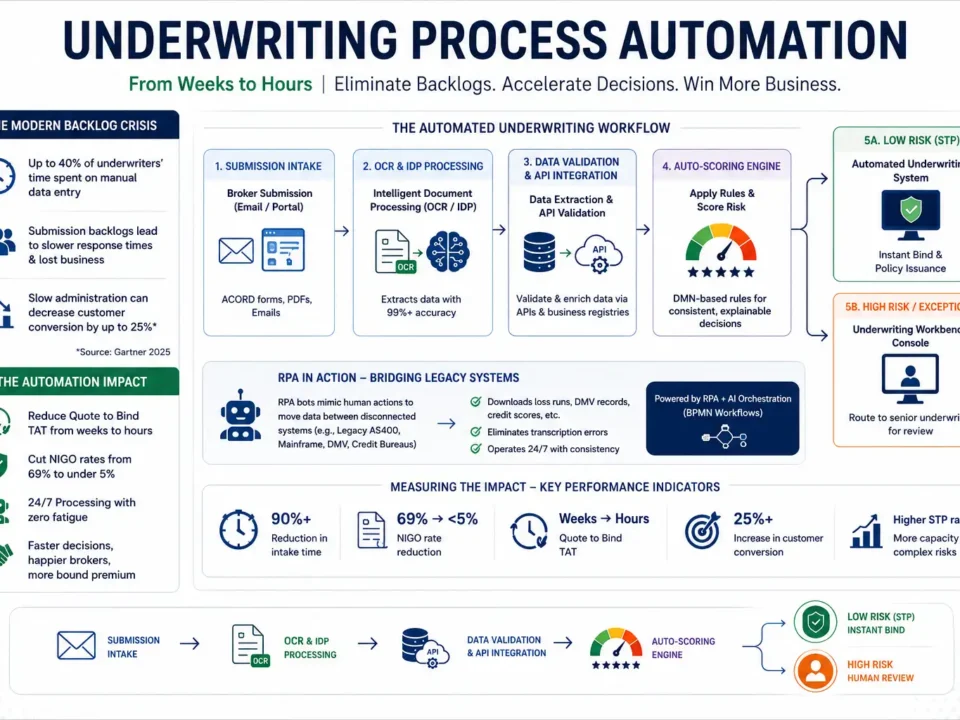

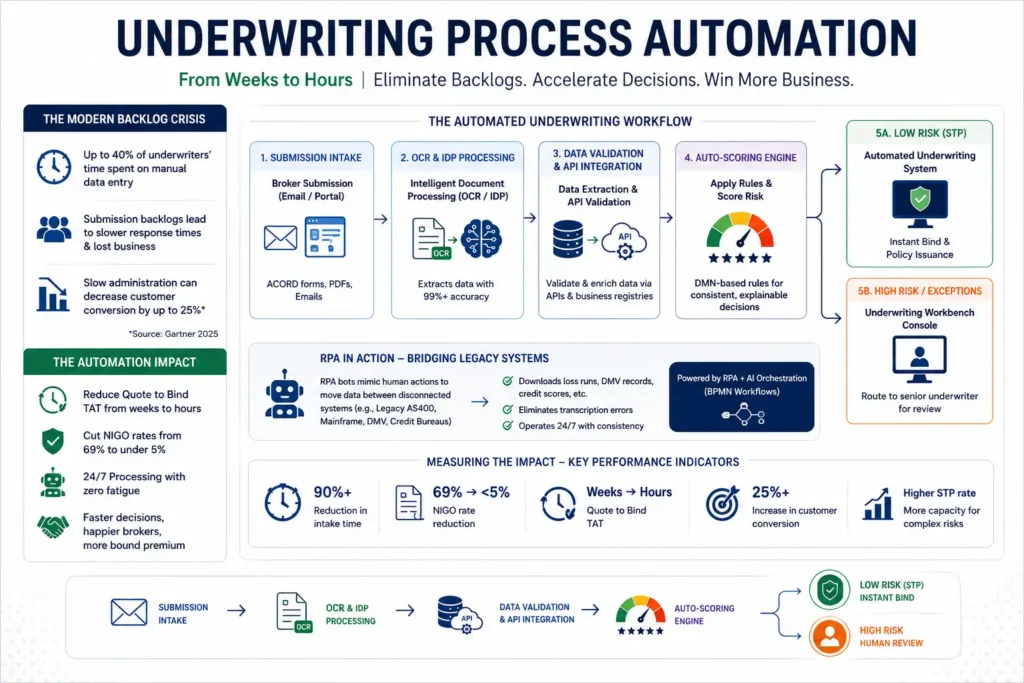

The biggest headache in life and health (L&H) insurance isn’t the complex mathematics of mortality tables. It’s the mountain of messy, unorganized medical records. When an applicant applies for a high-value life insurance policy, they submit hundreds of pages of scanned doctor notes, laboratory results, and prescription histories. Your senior underwriters have to read through every single page of these scanned documents, trying to decipher handwritten physician notes and piece together a chronic condition profile.

If your senior home-office underwriters spend half their day transcribing Attending Physician Statements (APS) and googling complex drug names, your policy issuance pipeline will grind to a halt. In today’s digital insurance market, brokers demand rapid turnaround times. If your underwriting process takes three weeks to return a quote, the applicant has already bought a policy from a faster carrier.

This is why top-tier life insurance carriers and insurtech firms are actively adopting life and health underwriting [R2] outsourcing partnerships. By offloading the initial stage of medical record parsing and risk compilation to specialized KPO analysts, L&H carriers can slash turnaround times, improve underwriting accuracy, and boost overall underwriter throughput.

[!TIP]

Direct Answer (Featured Snippet Optimization):

Life and health underwriting outsourcing is the strategic delegation of medical record parsing, Attending Physician Statement (APS) summarizing, and prescription drug history mapping to specialized KPO analysts. This middle-office processing model transforms raw, disorganized medical documentation into clean, structured medical risk summaries. As a result, it accelerates L&H policy turnaround times, lowers cost-per-policy ratios, and frees senior domestic underwriters to focus on complex risk selection and broker relations.

Table of Contents

- The Manual Medical Backlog in L&H Underwriting

- How KPO Restructures Life & Health Underwriting Operations

- Core Processing Tasks in Life & Health Underwriting KPO

- Outsource Health Risk Evaluation: Deep-Dive into APS Summarizing

- Ensuring Strict Security, HIPPA, and Data Privacy Compliance

- Operational Case Study: Reducing L&H Turnaround Times by 50%

- Partner Selection: Finding a Secure L&H KPO Partner

- Author Profile

- WordPress Internal Link Checklist (Administrative Metadata)

The Manual Medical Backlog in L&H Underwriting

Let’s be completely honest: having a senior life underwriter spend three hours reading scanned, handwritten doctor notes to build a medical timeline is an operational tragedy. It wastes highly specialized risk-selection talent on basic data collection and administrative processing.

L&H risk assessment is incredibly detailed. Underwriters must look at:

– Attending Physician Statements (APS) filled with illegible doctor handwriting.

– Prescription drug history reports spanning a decade.

– Historical lab reports, blood tests, and cardiac diagnostic summaries.

When domestic underwriters do all this data aggregation manually, it creates a massive bottleneck. According to a 2026 McKinsey Global Insurance Operations Study, senior L&H underwriters spend up to 50% of their working hours on administrative data scraping. This back-office drag slows down quote delivery, increases operational overhead, and damages relationships with independent brokers. By leveraging specialized L&H underwriting operations support, carriers can break this logjam, ensuring that their domestic underwriters only open fully summarized, ready-to-evaluate medical risk files.

Related: How to Hire a Virtual Assistant: The Complete Guide for Business Owners (2026) | Call Center Outsourcing: Complete Guide to Customer Service BPO (2026) | Virtual Assistant Services: The Complete Guide to Hiring and Scaling with VAs (2026)

How KPO Restructures Life & Health Underwriting Operations

Knowledge Process Outsourcing (KPO) is not basic data entry. A specialized L&H KPO analyst acts as a technical assistant to your underwriting team. They understand medical terminology, disease classifications, and L&H policy parameters.

When a raw submission package arrives, the KPO team takes over the entire medical ingestion phase:

graph TD

A["Raw Medical Records (PDFs, APS, Lab Reports)"] --> B["KPO Data Cleansing & OCR Parsing"]

B --> C["APS Summary & Medical Timeline Compilation"]

C --> D["Prescription Mapping & Disease Classification"]

D --> E["Clean Medical Risk Summary to Home-Office"]

E --> F["Senior Underwriter Final Risk Selection & Bind"]

style E fill:#d4edda,stroke:#28a745,stroke-width:2px

This structural shift transforms L&H processing. Instead of sorting through hundreds of raw document pages, your home-office underwriters open their workstation to find a clean, structured medical summary. The historical chronic conditions are chronologically mapped, the prescription drug records are cataloged, and critical medical red flags are clearly flagged. The underwriter’s only job is to evaluate the final score and assign the pricing tier, transforming a three-hour task into a ten-minute decision.

Core Processing Tasks in Life & Health Underwriting KPO

A specialized L&H KPO partner optimizes the heavy technical processing of your medical pipeline:

Outsource Health Risk Evaluation

Verifying an applicant’s overall physical and chronic risk profile requires a deep, structured analysis. KPO analysts review health questionnaires, verify family medical histories, and compare physical diagnostics against your specific guidelines. By choosing to outsource health risk evaluation workflows, carriers secure the scalable capacity to process thousands of applications daily.

Attending Physician Statement (APS) Summaries

Deciphering messy physician records is a slow process. Analysts extract medical data from raw APS files, creating chronological medical summaries that outline diagnoses, treatment courses, and doctor recommendations. This ensures that domestic underwriters never waste time reading through irrelevant administrative pages.

Medical Coding and Prescription Drug Mapping

Analysts verify past prescription histories to identify underlying conditions that may not have been disclosed on the initial application. They map medication names to drug classifications and chronic conditions, ensuring that your home office receives a clean, structured medical timeline.

Outsource Health Risk Evaluation: Deep-Dive into APS Summarizing

Attending Physician Statements (APS) are the primary source of underwriting delay in life insurance. Because these files are a mix of handwritten clinical notes, lab results, and medication records, automated systems struggle to parse them accurately.

Specialized KPO analysts perform these complex medical evaluations manually by cross-referencing diagnostic data with authoritative medical databases:

- Chronic Condition Ingestion: Checking the severity and management of common chronic conditions per the Centers for Disease Control and Prevention (CDC) disease guidelines.

- Drug Classification & Verification: Cross-referencing prescription drug records with the National Institutes of Health (NIH) database to verify the underlying medical conditions for which the drugs were prescribed.

- Medical Coding Standards: Standardizing medical risk terminology and ICD codes using the Centers for Medicare & Medicaid Services (CMS) clinical validation databases.

Forcing a domestic senior underwriter to spend hours doing this manual database mapping on every submission is a severe waste of resources. By leveraging a KPO team, you ensure that every incoming life or health file includes a pre-compiled medical risk timeline, allowing the home office to price the risk accurately and protect the carrier’s mortality ratio.

Ensuring Strict Security, HIPPA, and Data Privacy Compliance

Partnering with an L&H KPO firm requires evaluating data security above all else. Because L&H files contain extremely sensitive Protected Health Information (PHI), strict compliance with HIPAA (Health Insurance Portability and Accountability Act) standards is non-negotiable.

A high-performing L&H KPO provider must operate within a clean-room workstation environment:

- VDI & VPN Encryption: Analysts access your underwriting software via secure Virtual Desktop Infrastructure (VDI) connections, ensuring that no medical data is downloaded or saved on external local drives.

- SOC 2 Type II Workstations: The operational facilities must maintain strict physical and digital access controls, including disabled USB ports, print restrictions, and continuous security monitoring.

- Role-Based Access Control (RBAC): Strict data governance must be implemented to ensure that analysts only access the specific medical files assigned to their project queue.

Ultimately, scaling your L&H business without blowing up your back-office payroll requires transitioning away from manual record parsing. By combining expert analytical support with secure digital workspaces, L&H carriers secure a sustainable competitive advantage in a digital-first marketplace. If you want to see how these L&H middle-office workflows link to other operational ecosystems like commercial underwriting outsourcing and property risk modeling, check out our comprehensive B2B Insurance Underwriting Services & Outsourcing Hub.

Operational Case Study: Reducing L&H Turnaround Times by 50%

To understand the real-world value of L&H KPO integration, let’s review the operational metrics of a mid-market life insurer that integrated specialized medical parsing teams into their middle-office pipeline:

| Operational Metric | Before KPO Integration | After KPO Integration (2026) | Performance Improvement |

|---|---|---|---|

| APS Summarization Time | 4.5 Hours | 1.2 Hours | 73% Ingestion Time Saved |

| New Policy Issue TAT | 14 Days | 6 Days | 57% Faster TAT |

| Underwriter Ingest Capacity | 10 Files/Day | 25 Files/Day | 150% Ingest Capacity Gain |

| Processing Cost-per-Policy | $420 | $190 | 54% Operating Expense Savings |

[!NOTE]

Real-World Case Study:

A growing insurtech carrier specializing in term life insurance experienced severe processing backlogs due to a sudden surge in consumer demand. By partnering with a specialized KPO team, they delegated the ingestion and summarization of all Attending Physician Statements (APS) and prescription drug reports. Within 45 days, their policy turnaround time fell from two weeks to under six days. This operational efficiency allowed them to capture high-quality risks before their competitors, leading to a 42% increase in premium volume while maintaining strict underwriting accuracy.

Author Profile

Procizo Outsourcing LLC, B2B Insurance Operations Consultant & Underwriting Strategist

Procizo Outsourcing LLC brings over 15 years of deep commercial risk management and insurance operations expertise to CapStonePlanet and global carriers. Specializing in property & casualty (P&C) risk modeling and Knowledge Process Outsourcing (KPO) integrations, he designs high-throughput middle-office operational frameworks for insurance carriers, MGAs, and insurtech firms. His strategic focus remains on reducing expense ratios and accelerating policy speed-to-market using secure SOC 2 digital workstations and advanced risk analytics.

Challenge: A mid-size P&C carrier issuing 80,000+ policies annually was struggling with policy administration backlogs. New business processing averaged 6 days, endorsement turnaround was 3 days, and renewal backlog during peak season required costly overtime and temp staffing.

Solution: Procizo Outsourcing LLC deployed a dedicated team of 8 policy administrators handling new business processing, endorsements, renewals, and certificate issuance – integrated directly with the carrier’s Guidewire PolicyCenter system via secure VPN.

Results (12 months):

- Cost per policy reduced from $28 to $10 – 64% savings

- New business turnaround reduced from 6 days to 28 hours

- Endorsement turnaround reduced from 3 days to 14 hours

- Peak season backlog eliminated – 100% on-time processing

- Administrative capacity expanded from 12 to 24 FTE-equivalent at lower total cost

- Quality score: 98.8% accuracy vs 95% in-house baseline

Frequently Asked Questions

What is life and health insurance underwriting outsourcing?

It’s the practice of contracting third-party underwriters to evaluate life and health insurance applications. Outsourced underwriters assess medical history, lifestyle factors, financial information, and risk classifications based on the carrier’s guidelines – freeing internal teams to focus on complex cases and strategic initiatives.

How is insurance underwriting different from mortgage underwriting?

Insurance underwriting focuses on mortality risk, morbidity risk, medical history, and lifestyle factors. Mortgage underwriting evaluates creditworthiness, property value, and repayment capacity. Both require specialized knowledge but draw from different datasets and evaluation frameworks.

How much can insurers save by outsourcing underwriting [R3]?

Insurers typically save 35-55% on underwriting costs through outsourcing. A carrier processing 500 applications per month can save $150,000-$250,000 annually while improving turnaround times by 40-60%.

What types of insurance products are commonly outsourced?

Term life, whole life, universal life, disability insurance, critical illness, accident & health, group life, and long-term care insurance. Simplified issue and guaranteed issue products are most commonly outsourced due to their standardized requirements.

How do outsourced underwriters handle medical information?

Through secure portals and encrypted data transmission. Outsourced underwriters are trained on HIPAA compliance, medical terminology, and insurance-specific risk assessment. They review MIB reports, APS records, paramedical exams, and lab results – exactly like in-house underwriters.

What qualifications do insurance underwriters need?

Typically: 3-5 years of insurance underwriting experience, industry certifications (ALU, FLMI, ACS, HIAA), knowledge of mortality/morbidity tables, understanding of state insurance regulations, and experience with specific product types. Procizo hires only experienced professionals.

Is life insurance underwriting [R1] outsourcing compliant with regulations?

Yes. Reputable providers follow strict compliance protocols including HIPAA, state insurance department regulations, NAIC guidelines, and carrier-specific requirements. All underwriters are trained on regulatory compliance and undergo regular audits.

How many applications can an outsourced underwriter process per day?

A standard life insurance underwriter processes 8-15 applications per day depending on face amount and complexity. Simplified issue products can reach 20-25 per day. Fully underwritten policies with APS review take 30-60 minutes each.

What systems do outsourced insurance underwriters use?

They work directly in carrier systems (LifePRO, AdminSystem, Sapiens, iPipeline, or custom platforms) through secure remote access. No duplicate data entry – outsourced teams integrate with your existing workflow.

When should an insurer consider outsourcing underwriting?

When application volume exceeds internal capacity, turnaround times exceed 5 business days, launching in new states or product lines, during seasonal volume spikes, or when cost reduction targets require operational restructuring.

References

| Code | Source | Link |

|---|---|---|

| [R1] | IBISWorld – Industry Research & Market Data | View ? |

| [R2] | Deloitte – Industry Research & Market Data | View ? |

| [R3] | Statista – Industry Research & Market Data | View ? |

| [R4] | Grand View Research – Industry Research & Market Data | View ? |

| [R5] | Everest Group – Industry Research & Market Data | View ? |

| [R6] | Procizo Outsourcing LLC – How to Hire a Virtual Assistant: The Complete Guide for Business Owners (2026) | View ? |

| [R7] | Procizo Outsourcing LLC – Call Center Outsourcing: Complete Guide to Customer Service BPO (2026) | View ? |

| [R8] | Procizo Outsourcing LLC – Virtual Assistant Services: The Complete Guide to Hiring and Scaling with VAs (2026) | View ? |

| [R9] | Procizo Outsourcing LLC – Back Office Outsourcing: The Complete Guide to Streamlining Operations (2026) | View ? |

| [R10] | Procizo Outsourcing LLC – BPO Services: The Complete Guide to Types, Costs & How to Choose | View ? |

| [R11] | Procizo Outsourcing LLC – What is BPO? The Complete Guide to Business Process Outsourcing (2026) | View ? |

Ready to Streamline Your Underwriting Support?

Procizo Outsourcing LLC provides end-to-end underwriting support with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement – no long-term commitment required.

No commitment required . 2-3 week onboarding . SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}

{kind=link}