- Have Questions? Talk to Us

- info@procizo.com

Underwriting Process Automation: Carrier Efficiency Guide

Agentic AI in Insurance Underwriting: 2026 Guide

June 15, 2026

Direct Answer:

Underwriting process automation uses software technologies like robotic process automation (RPA), optical character recognition (OCR) and APIs to ingest, scrub and validate applicant risk data automatically. Consequently by eliminating manual transcription and legacy workflow bottlenecks, this technology drastically improves underwriting workflow efficiency. Furthermore it allows carriers to reduce quote to bind turnaround times (TAT) from weeks to hours while human underwriters focus on complex risks.

Modern insurance carriers face a critical operational challenge submission backlogs specifically, brokers submit thousands of ACORD applications daily but traditional manual verification systems cannot keep pace. As a result carrier teams spend up to 40% of their workdays on manual data entry rather than actual risk analysis. To solve this problem forward thinking insurers are implementing underwriting process automation. This technical shift eliminates administrative bottlenecks. Ultimately, integrating these automated workflows allows carriers to protect broker relationships and win high value accounts.

Table of Contents

- The Modern Backlog Crisis

- Automating the Intake Funnel via OCR and APIs

- Robotic Process Automation (RPA) in Action

- Automating the Risk Evaluation Process

- Measuring the Impact: Key Performance Indicators

- Scenario Case Study: Resolving a 45-Day Backlog

- Executive Summary

- Frequently Asked Questions (People Also Ask)

- Author Profile

- WordPress Internal Link Checklist (Administrative Metadata)

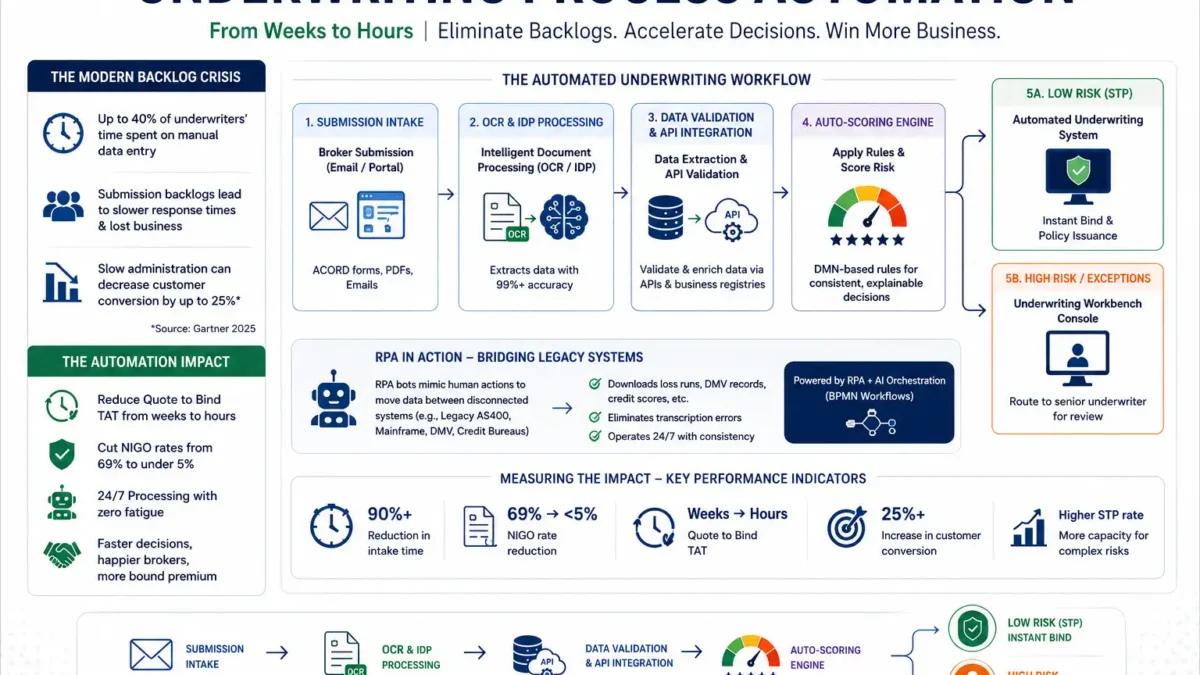

The Modern Backlog Crisis

Historically , traditional underwriting models relied heavily on manual data retrieval. For instance staff had to manually query multiple databases to gather loss history, property deeds and credit scores. Because of this fragmented workflow, applications sat in queues for several days before a human even opened them. Consequently this delay frustrated broker partners who quickly diverted premium accounts to faster competitors.

Furthermore recent 2025 research from Gartner shows that administrative delay is the single largest driver of carrier friction specifically slow response times directly decrease customer conversion rates by up to 25%. Therefore insurers must transition away from legacy data entry processes to protect their market share.

By upgrading to modern insurance underwriting software technology, companies can establish a smooth, high throughput pipeline. This transformation resolves the backlog crisis and establishes a baseline for long term growth.

Automating the Intake Funnel via OCR and APIs

To improve underwriting workflow efficiency, carriers must automate document ingestion at the front of the funnel. Specifically modern platforms utilize intelligent document processing (IDP) powered by optical character recognition (OCR) and natural language processing (NLP). These advanced systems scan incoming emails, PDFs, and ACORD forms to extract vital applicant data instantly.

For instance IBM analytics indicate that IDP engines extract structured data with over 99% accuracy. Consequently this technology reduces Not in Good Order (NIGO) submissions from a typical 69% error rate to under 5%. As a result software eliminates manual keystrokes entirely. Once the software extracts the data the platform transmits this structured data via secure APIs directly into the core underwriting workbench software.

Meanwhile validation scripts immediately cross-reference the tax IDs and business registries to check for errors. Consequently, underwriters receive clean, verified files that are ready for immediate review. By automating the intake funnel, carriers completely bypass the manual scrubbing stage, cutting intake times from hours to seconds.

Robotic Process Automation (RPA) in Action

While APIs connect modern systems legacy carrier databases often lack direct integration capabilities. In these situations, insurers deploy robotic process automation insurance software to bridge the technical gap. Specifically RPA bots mimic human user actions to transfer data between disconnected applications, such as a legacy AS400 mainframe and a modern cloud database.

Furthermore these software robots execute repetitive tasks with absolute consistency. For example they automatically download loss run histories, pull DMV records and paste credit ratings into risk templates. Because RPA bots operate 24/7 without fatigue, they eliminate transcription errors and significantly accelerate processing speeds.

In addition carriers can deploy RPA alongside newer agentic AI insurance underwriting systems. In this hybrid setup, Business Process Model and Notation (BPMN) orchestration maps the workflows. Consequently the RPA bot performs the manual data movement, while the AI agent makes cognitive decisions. Ultimately, this combination allows carriers to automate complex workflows without completely rebuilding their legacy core systems.

Automating the Risk Evaluation Process

Beyond simple document intake, carriers must also automate risk evaluation process mechanics to achieve true operational scale. Specifically, automation engines apply pre-defined underwriting rules directly to the ingested applicant data. To ensure auditability and compliance, these engines utilize Decision Model and Notation (DMN) tables. Consequently, they keep a clear, explainable record of why the system approved or flagged a risk, avoiding the “black box” trap that concerns regulators.

Furthermore, these engines apply specific rules depending on the domain. For instance, in insurance underwriting, the engine evaluates property hazard histories, driving records, and liability classifications. Conversely, in loan underwriting, the system focuses on debt-to-income (DTI) calculations, credit scores, and collateral valuations.

Consequently, for standard, low-complexity risks, the automated insurance underwriting systems can calculate the final score and price the policy instantly. Conversely, if the application violates a specific risk threshold, the engine automatically flags the exception. The system then routes the file to a senior underwriter via a modern cloud insurance underwriting software dashboard.

Moreover, this automated routing prevents high-risk applications from slipping through the cracks. In other words, the technology acts as a smart gatekeeper. By automating the screening layer, senior team members only focus on files that require human experience and relationship management. Therefore, the carrier maximizes its technical resources while keeping loss ratios low.

Measuring the Impact: Key Performance Indicators

To justify the investment in automation, insurance executives must track specific business metrics. Specifically, carriers measure turnaround time (TAT) reduction, straight-through processing (STP) rates, and employee satisfaction. When insurers implement process automation, they typically see quote-to-bind times drop from days to minutes.

Furthermore, according to data from Deloitte, automation reduces processing costs by up to 50% while improving data accuracy. In addition, eliminating manual data entry improves underwriter morale, since staff can focus on strategic tasks rather than administrative chores.

Consequently, the overall loss ratio improves because automated systems apply rating rules with 100% consistency. Unlike humans, software never skips a verification step due to fatigue. Ultimately, tracking these KPIs allows carriers to continuously optimize their workflows and maintain a high-performance operation.

Key Performance Metrics: Before vs. After Process Automation

| Operational Metric | Manual Underwriting | Automated Underwriting Process | Performance Impact |

|---|---|---|---|

| Data Intake Speed | 45-60 Minutes / File | Under 2 Minutes / File | 95%+ Time Saved |

| Data Extraction Accuracy | ~88% (Human Errors) | 99.5% (OCR + API Checks) | Reduced Underwriting Leakage |

| Straight-Through Processing (STP) | 0% (All Manual Review) | 65% – 80% (Standard Risks) | Drastic Workflow Acceleration |

| Average Quote Turnaround Time | 5 – 10 Business Days | Under 4 Hours | Enhanced Broker Satisfaction |

| Average Processing Cost | $250 – $400 / Policy | $45 – $80 / Policy | Up to 80% Operational Savings |

Scenario Case Study: Resolving a 45-Day Backlog

To understand the real-world value of these technologies, let’s examine a mid-sized commercial property insurer that faced a severe backlog. Specifically, during the Q4 renewal surge, the carrier experienced a 45-day delay in binding new quotes. Because of this bottleneck, the company lost major broker partners and saw its conversion rate drop by 30%.

Consequently, the leadership team deployed an integrated automation framework. The setup combined intelligent OCR intake with RPA bots to query legacy platforms. As a result, the carrier automated the intake of ACORD 125 and ACORD 140 forms.

Ultimately, the results were dramatic. Within 30 days of implementation, the insurer eliminated its entire backlog. Furthermore, the quote-to-bind turnaround time fell from 12 days to just 3 hours. Because of this speed-up, the carrier bound $5.2 million in new annual premium while maintaining a flat operational headcount. This success story proves that process automation is a critical competitive advantage for modern carriers.

[!NOTE]

Operational Success Spotlight:

A specialty cargo insurer integrated robotic process automation to connect their modern Salesforce CRM with a legacy AS400 rating mainframe. Before automation, underwriters manually copied 42 data points per application. Consequently, they processed only 8 submissions daily. After deploying RPA bots to transfer data, processing capacity surged to 65 files per day, and underwriting data entry errors dropped to zero.

Executive Summary

To summarize, modern carriers must adopt automation to survive in a highly competitive market. Specifically, the key takeaways include:

– Intake Speed: Automated document processing cuts file ingestion from hours to seconds.

– RPA Bridges: Robotic software connects modern applications to legacy systems without expensive IT overhauls.

– Error Reduction: APIs and OCR engines eliminate human transcription errors and data leakage.

– Underwriter Focus: Automation handles repetitive administrative tasks, allowing senior underwriters to concentrate on broker relationships and complex risk management.

– Improved Margins: Lower processing costs and higher quote speeds directly drive carrier profitability.

Frequently Asked Questions (People Also Ask)

1. What is underwriting process automation?

Specifically, it is the use of digital tools like RPA, OCR, and APIs to ingest, scrub, and validate applicant risk data. Consequently, this technology reduces manual tasks and increases operational speed.

2. How does RPA help in insurance underwriting?

For instance, RPA bots transfer data between legacy mainframes and modern cloud databases. Therefore, they eliminate manual copy-pasting and prevent data entry errors.

3. What is the difference between RPA and Agentic AI in underwriting?

In comparison, RPA follows strict, rule-based workflows to move data. Conversely, agentic AI makes cognitive decisions, like evaluating risk summaries or asking for missing documents.

4. Can process automation improve carrier loss ratios?

Indeed, automation ensures that risk engines apply pricing rules with 100% consistency. As a result, the carrier avoids underpricing risks due to human fatigue or oversight.

5. How long does it take to implement robotic process automation in insurance?

Typically, carriers can deploy simple RPA bots within 4 to 8 weeks. However, connecting complex systems requires deep integration with core platform APIs.

6. What is underwriting workflow efficiency?

Ultimately, it is the ratio of processed applications to the time and cost spent. High efficiency means the carrier binds policies quickly with minimal administrative overhead.

Author Profile

Written by the CapStonePlanet Insurtech Editorial Team

Specialists in Enterprise Insurance Underwriting & AI Automation

Our team consists of veteran insurance tech analysts and software architects. Specifically, we specialize in turning complex insurtech trends—like Agentic AI, straight-through processing (STP), and core systems modernization—into simple, actionable steps. With decades of experience consulting for top P&C and L&H carriers, we help firms leverage underwriting process automation to reduce expense ratios, eliminate backlogs, and accelerate policy speed-to-market.

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}

{kind=link}