- Have Questions? Talk to Us

- info@procizo.com

Agentic AI in Insurance Underwriting: 2026 Guide

What Is MCA Underwriting? The Complete Process for Funders (2026)

June 9, 2026

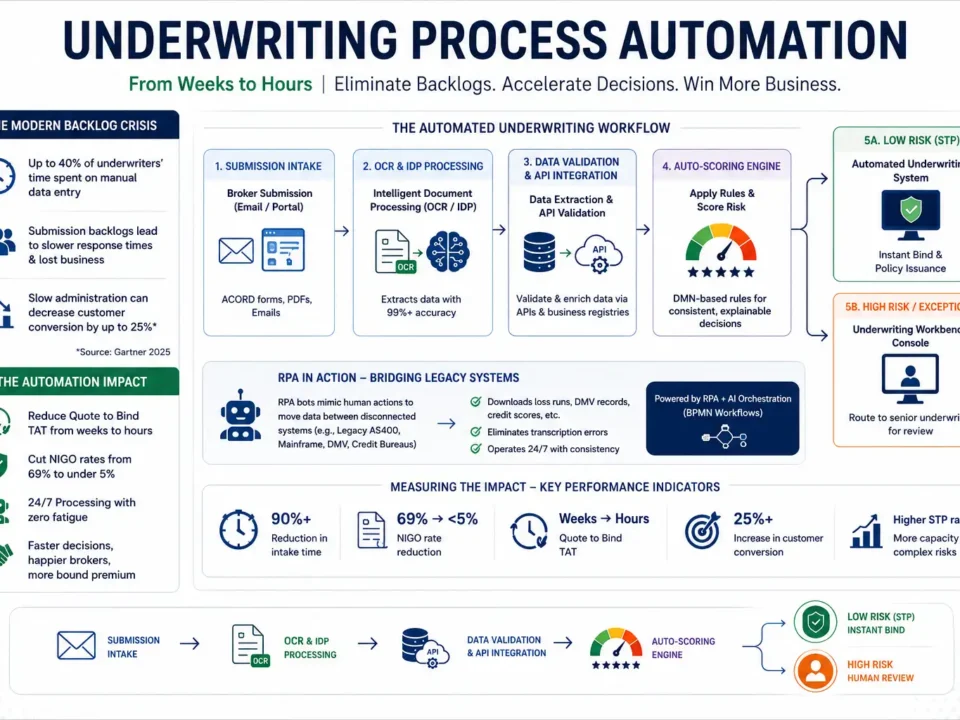

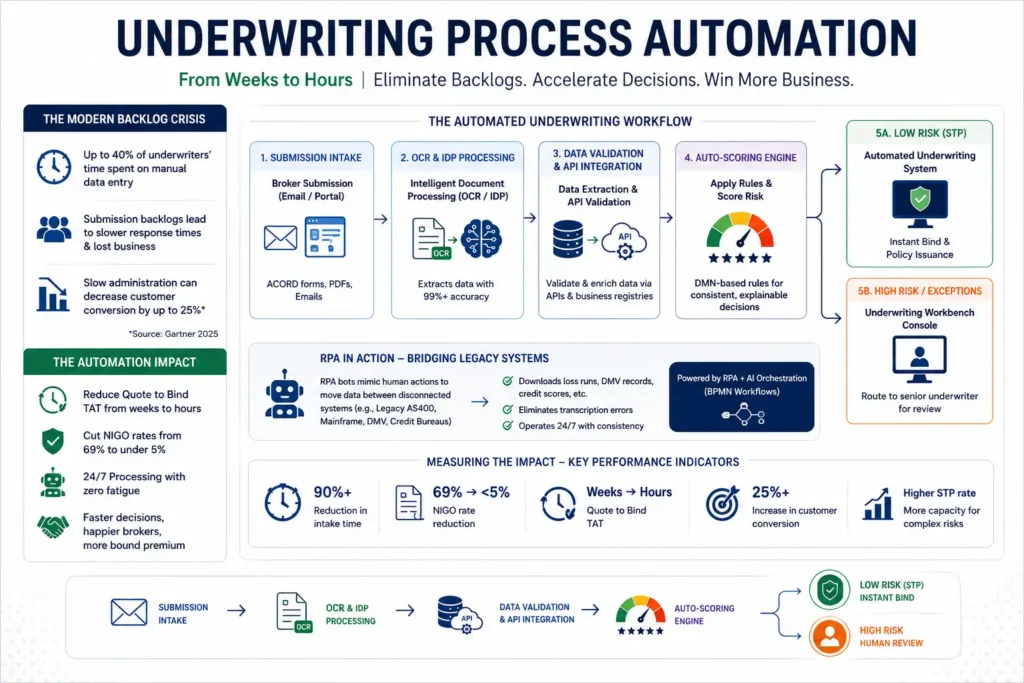

Underwriting Process Automation: Carrier Efficiency Guide

June 15, 2026

Direct Answer:

Agentic AI in insurance underwriting means smart systems that complete complex risk checks on their own. Unlike basic AI, these agents pull data, find errors, and act as advanced automated insurance underwriting systems. Consequently, they process standard policies instantly. This lets human underwriters focus only on the hardest cases.

When carriers first tried AI in insurance, they mostly used it to write emails or summarize records. While it was useful, this approach didn’t solve the main problem.

In fact, according to McKinsey, admin tasks still eat up 30-40% of an underwriter’s time. This proves that simple automation isn’t enough.

Therefore, modern insurance underwriting software technology is changing how we look at risk. Instead of waiting for a human to click a button, advanced artificial intelligence underwriting systems act as a “digital underwriter.”

Specifically, these smart systems automate tasks by:

– Watching for new submissions from ACORD forms and emails.

– Pulling messy data from broker portals.

– Checking early scores against NAIC rules.

– Sending the file to a human only when there is a major issue.

Furthermore, this is happening right now. According to Gartner, by 2028, 33% of business apps will include agentic AI.

Agentic AI Underwriting Statistics

Carriers that use these autonomous AI underwriting systems are already seeing massive changes:

- 60% faster time to bind a quote.

- 30–40% less admin work for senior staff.

- 70%+ straight-through processing (STP) rates for simple small business policies.

- 3–5% better loss ratios because of highly accurate risk checks.

- Faster turnarounds, dropping from days to minutes.

Real Underwriting Workflow Examples

Indeed, the real power of agentic AI shines when you look at daily tasks on the floor:

- SME Business Insurance: For instance, the system can quickly check low-risk retail apps, verify ACORD 130 data, run background checks, and issue a quote with zero human help.

- Commercial Auto: Similarly, the AI agent connects to driving databases to check fleet history. If the data matches, it processes the policy. Conversely, if there is a big problem, the system alerts a human.

- Workers Compensation: Meanwhile, the system automatically compares the employer’s payroll data against state tax records. It only flags high-risk payroll errors.

The 4-Layer Agentic Underwriting Stack

To build a fully automated underwriting process automation pipeline, tech leaders use a setup known as the 4-Layer Agentic Stack.

Layer 1: The Intake Agent

Monitors email inboxes and broker portals. It extracts data from PDFs and loss runs.

Layer 2: The Validation Agent

Checks the extracted data against core systems (like Guidewire or Duck Creek) to ensure it is clean.

Layer 3: The Risk Scoring Agent

Applies the carrier’s specific rules to price the policy accurately.

Layer 4: The Compliance Oversight Agent

Makes sure the decision follows all state laws before finalizing the quote.

The Reality of Implementation: Friction and Failures

Vendors often sell Agentic AI as an easy fix. However, this is a dangerous trap. In reality, most carriers are not ready for it.

Consequently, the truth on the floor looks like this:

– Old System Failures: If your data lives in 1990s mainframes, the AI agent will fail. Ultimately, old data tech is the biggest roadblock.

– Messy Data: Furthermore, AI makes bad choices when it learns from messy or missing loss histories.

– Underwriter Distrust: Underwriters trust their gut instinct. Thus, asking them to trust a machine requires a massive culture shift.

– IT vs. Underwriting Conflict: Additionally, IT teams want to move fast, while underwriters demand perfect accuracy. This causes internal fights.

– Governance Issues: Finally, running AI without strict rules creates massive legal risk.

Comparison: Enterprise Underwriting Models

| Metric | Traditional Underwriting | Basic Generative AI | Agentic AI Systems |

|---|---|---|---|

| Workflow Execution | 100% Human | Human-prompted | Autonomous |

| Governance Complexity | Low | Moderate | Extremely High |

| Integration Burden | None | Low (API to LLM) | High (Core System APIs) |

| Underwriter Resistance | N/A | Low | High |

| Auditability | Manual notes | Chat logs | Immutable Ledger Logs |

Agentic AI Adoption Maturity Model

Where does your carrier stand? Most companies fall into Level 1 or 2.

Level 1: AI Assistance

Underwriters use chatbots to summarize documents. A human does 100% of the actual work.

Level 2: Workflow Automation

Basic rules route emails and pull data, but humans still make all decisions.

Level 3: Partial Autonomy

At this stage, AI handles data entry. It presents a pre-filled underwriting workbench software for human review.

Level 4: Human-Supervised Autonomous Underwriting

Subsequently, the tech handles the whole process for simple risks (like SME). It only stops for complex exceptions.

Level 5: Continuous Adaptive Underwriting

Ultimately, the system uses predictive analytics in insurance underwriting via IoT sensors. It adjusts portfolio risk in real-time without human input.

The Future of Human-in-the-Loop

The fear that AI will steal underwriting jobs is largely wrong. Instead, human oversight will stay mandatory for complex commercial risks.

By dropping manual data entry, underwriters can shift to managing hard exceptions, broker relations, and high-level strategy. Therefore, modern cloud insurance underwriting software acts as the critical bridge between the AI’s speed and human judgment.

Executive Summary: The Reality of Autonomous Underwriting

- What it changes: This tech shifts underwriting from manual data entry to strategic risk management.

- What carriers misunderstand: Many wrongly think these tools are plug-and-play. On the contrary, success requires pristine data lakes and deep integration with core systems like Duck Creek.

- Where ROI is realistic: Currently, the best returns are in high-volume, simple lines like SME, basic workers’ comp, and standard commercial auto.

- Why human oversight matters: Above all, AI cannot replace relationship building with brokers or the nuanced judgment needed for large commercial risks.

Frequently Asked Questions (People Also Ask)

1. Will AI replace insurance underwriters?

No. Agentic AI takes over basic admin tasks like data entry. Human underwriters shift to managing complex cases, broker relationships, and high-level strategy.

2. What is straight-through processing (STP) in underwriting?

STP is a fully automated workflow. An insurance application is received, analyzed, priced, and bound entirely by software—without any human touch.

3. How does agentic AI differ from generative AI?

Generative AI creates content, like summarizing a 50-page file, based on a human prompt. Agentic AI acts on its own. It requests missing documents, checks data, and runs scores without needing a human trigger.

4. Can AI automatically approve insurance policies?

Yes, but usually only for simple, high-volume policies like small business or basic auto insurance. The risk profile must fit perfectly within the carrier’s automated rules.

5. How do insurers prevent AI underwriting bias?

Carriers build “explainable AI” systems. These multi-agent setups keep a secure, clear log of every data point pulled and every choice the AI made. This ensures they follow fair lending and NAIC laws.

6. What are the risks of autonomous underwriting systems?

The main risks include bad decisions caused by messy training data, massive integration failures with old mainframes, and legal fines if the AI’s logic cannot be clearly audited.

About the Author

Written by the CapStonePlanet Insurtech Editorial Team

Specialists in Enterprise Insurance Underwriting & AI Automation

Our team consists of veteran insurance tech analysts and software architects. With decades of experience consulting for top P&C and L&H carriers, we specialize in turning complex insurtech trends—like Agentic AI, straight-through processing (STP), and core systems modernization—into simple, actionable steps.

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}