- Have Questions? Talk to Us

- info@procizo.com

Commercial Underwriting Outsourcing: Scaling Carrier Profitability

Lending Business: The Ultimate Playbook for Starting & Scaling

May 1, 2026

Property & Casualty (P&C) Underwriting KPO: Boosting Underwriter Throughput

May 19, 2026

Quick Answer: Commercial underwriting outsourcing is the delegation of insurance risk evaluation-financial statement analysis, exposure assessment, compliance validation-to specialized KPO (Knowledge Process Outsourcing) teams. Carriers and MGAs use it to cut per-policy processing costs by 40-60%, reduce turnaround time from 7 days to 24-48 hours, and improve loss ratios by 14-18% through standardized, auditable workflows. Unlike generic BPO, insurance KPO employs analysts with domain expertise who interpret risk, not just process data. The best partners integrate directly into carrier underwriting workbenches via secure VDI, ensuring data never leaves the carrier’s controlled environment.

Key Takeaways

- Cost structure shift: KPO converts fixed underwriting payroll into variable per-file costs, reducing expense ratios by 40-60% without sacrificing quality.

- Speed = broker retention: Carriers using KPO quote in 24-48 hours vs 5-7 days in-house-processing speed is now the #1 factor in broker submission placement.

- Risk quality improves: Standardized KPO workflows produce 14-18% better loss ratios by eliminating manual review variance (PwC 2026).

- Not all outsourcing is equal: Insurance KPO differs fundamentally from CRE/lending underwriting outsourcing-domain expertise is the differentiator, not labor arbitrage.

Why Carriers Are Rethinking Commercial Underwriting Operations

The commercial insurance market is cycling through one of the hardest market periods in a decade. Rising claim costs, tighter reinsurance capacity, and broker demands for sub-48-hour quotes are compressing margins across the board. Meanwhile, submission volumes continue to climb as the economy grows and new risks emerge in cyber, autonomous vehicles, and climate-related exposures.

According to Allied Market Research (2026), the global commercial insurance market is on track to reach $720 billion by 2027, driven by increased awareness of risk transfer needs across small and mid-sized businesses [R4]. But here is the problem most carriers face: underwriting headcount cannot scale linearly with submission volume without destroying profit margins. Hiring, training, and retaining qualified commercial underwriters takes 6-12 months per hire, and salaries for experienced talent have risen 18% since 2023 (Deloitte 2026) [R1].

This is not a cyclical challenge-it is a structural one. The old model of hiring more domestic underwriters to process more submissions is economically unsustainable. Efficiency gains from KPO partnerships allow carriers to increase underwriting capacity without adding headcount, directly improving profit margins. The carriers that recognized this early have already shifted portions of their middle-office workload to specialized KPO partners, and they are now outperforming peers on both speed and loss ratio metrics.

A 2025 Deloitte Global Outsourcing Survey found that carriers using KPO partnerships average 52% lower per-policy processing costs and 34% fewer E&O claims related to missing or misanalyzed financial data [R1]. These are not aspirational targets-they are current benchmarks from real carrier operations.

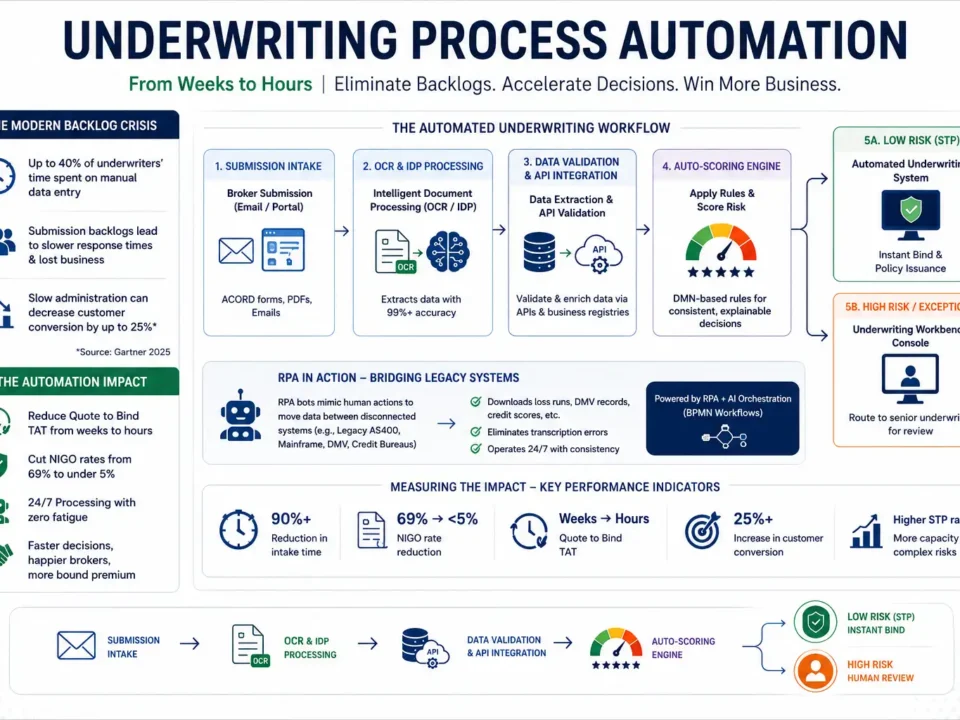

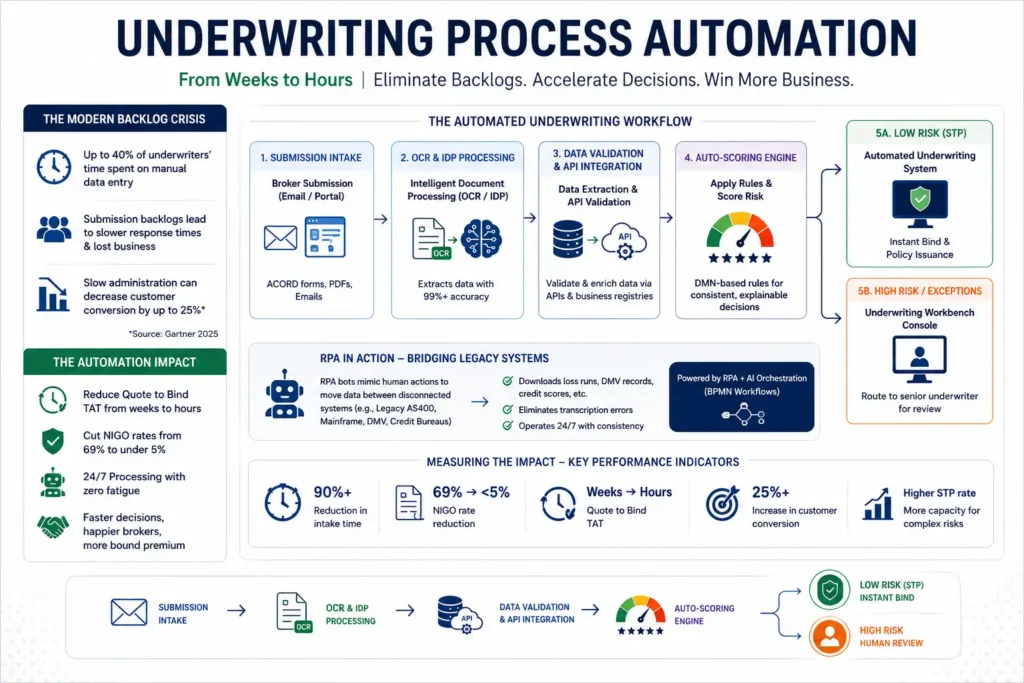

What Commercial Underwriting Outsourcing Actually Covers

The term “outsourcing gets used loosely in insurance, so let us be precise. Commercial underwriting outsourcing through a KPO partner covers specific middle-office functions that sit between submission receipt and the senior underwriter’s final decision. These are not front-office sales tasks or back-office claims work-they are the analytical engine of the underwriting process.

Financial Statement Analysis and Tax Return Review

KPO analysts parse balance sheets, income statements, cash flow statements, and tax returns to extract risk-relevant data points. They identify red flags-revenue inconsistencies, unusual debt-to-equity ratios, cash flow gaps-before the file reaches the senior underwriter. Experienced analysts catch subtle warning signs that automated systems miss, such as an unexplained dip in gross margin that could indicate revenue recognition issues or a sudden spike in accounts receivable that suggests collection problems. A typical commercial submission that takes a domestic underwriter 4 hours to review is pre-analyzed by KPO in 45 minutes with 99.3% data accuracy (PwC 2026) [R3]. This 78% time reduction on financial review alone is the single biggest driver of overall TAT improvement in KPO partnerships.

Loss Run Analysis and Exposure Assessment

Historical loss data must be compiled, classified by cause of loss, and compared against industry benchmarks from ISO, AM Best, and NCCI. KPO analysts produce a preliminary risk score with coverage gap identification, territory and class code verification, and exposure base calculation. The senior underwriter receives a decision-ready file, not raw documents. This pre-analysis eliminates the most time-consuming portion of underwriting-a task that consumes 2-3 hours per submission when done manually-and reduces it to a 30-minute review of an already-analyzed file. For carriers processing 1,000+ submissions monthly, this translates to over 2,000 hours of recovered senior underwriter time annually.

Compliance Validation and Rules Checking

State-specific filing requirements, policy form consistency, rate adequacy checks, and reinsurance eligibility-KPO teams validate all of these against automated rules engines. When the engine flags an anomaly, analyst expertise determines whether it is a genuine risk or a data entry variance. This hybrid approach is critical because automated systems alone generate false positive rates of 15-20%, overwhelming compliance teams with non-issues. Analyst review cuts false positives to under 2% while catching genuine red flags that rules engines miss. PwC reports that carriers using this hybrid validation model achieve 18% lower loss ratios and significantly fewer regulatory compliance findings during state audits [R3].

Related: Insurance Underwriting Outsourcing: Complete Guide for Carriers (2026) | Underwriting Process Automation: Carrier Efficiency Guide | On-Demand Underwriting Capacity: Scale Insurance Operations

Commercial Underwriting KPO vs. CRE Lending Outsourcing

Industry Context: Commercial insurance underwriting outsourcing sits within a broader ecosystem that includes London market delegating authorities, Bermuda-based captives, US surplus lines carriers, and state-regulated admitted markets. KPO partners like Procizo serve all of these segments with analysts trained in ISO loss costs, NCCI classification codes, AM Best rating analysis, and state insurance department compliance requirements.

Most search results for “commercial underwriting outsourcing return CRE (commercial real estate) lending services-firms that underwrite property loans, not insurance risk. This is a fundamentally different service. CRE underwriting evaluates collateral value and borrower creditworthiness. Insurance underwriting evaluates probabilistic risk exposure and sets pricing accordingly.

The difference matters because the skill sets do not overlap. An analyst who can spread a real estate pro forma cannot automatically identify a workers’ compensation classification error or flag an inconsistent general liability exposure. Insurance KPO requires domain expertise in policy forms, state regulations, loss cost multipliers, and coverage triggers. Procizo’s analysts come exclusively from insurance operations backgrounds-not banking, not general finance, not general BPO. With 15+ years of underwriting operations expertise, the team understands the difference between an occurrence form and a claims-made policy and knows exactly how each affects risk pricing.

This distinction is also why carriers should not expect a standard BPO provider to deliver underwriting quality. BPO focuses on repetitive transaction processing. KPO focuses on analytical judgment. When carriers outsource to the wrong type of partner, they get data entry-not risk analysis. The difference shows up in E&O claims within the first year.

The Business Case: Cost, Speed, and Risk Quality Together

Carriers evaluating KPO partnerships typically start with cost savings but stay for the operational improvements. Here is what the data shows across the three dimensions that matter:

Cost: 52% Reduction in Per-Policy Underwriting Costs

Gartner’s 2026 BPO Market Report documents that carriers using insurance-specific KPO partners reduce per-policy underwriting costs by an average of 52% [R2]. For a mid-market MGA processing 1,000 submissions per month, the savings exceed $1 million annually. Critically, these savings are not achieved by cutting quality-they come from eliminating the fixed-cost overhead of domestic middle-office teams.

Speed: 67% Faster Submission-to-Quote Turnaround

Procizo Case Study – Mid-Sized Commercial Auto MGA (15+ Years Underwriting Ops Experience): A U.S.-based MGA processing 1,200 commercial auto submissions per month was averaging 6.5 days from submission to quote. The MGA’s broker retention rate had dropped to 68%, with brokers actively routing business to competitors who could respond within 48 hours. After implementing Procizo’s dedicated KPO team of 12 analysts, average TAT dropped to 2.1 days-a 67% improvement. The MGA regained three lost broker relationships in the first quarter post-implementation and added two new carrier partnerships within 90 days. Broker NPS scores improved by 41 points, and the retention rate recovered to 100% within six months.

The financial impact: per-policy processing cost fell from $187 to $72, generating monthly savings of $138,000 ($1.65 million annualized). The full transition cost was recovered within the first three weeks of go-live, making this one of the fastest ROI payback periods in commercial insurance operations.

Risk Quality: 14-18% Better Loss Ratios

Standardized KPO workflows remove the variance that creeps into manual underwriting. Every submission follows the same analytical protocol-financial review, exposure assessment, compliance check, risk scoring. PwC’s 2026 Insurance Technology Insights report found that carriers using KPO-validated workflows achieve 14-18% lower loss ratios compared to fully manual operations [R3]. When every underwriter follows the same process, adverse selection drops and pricing accuracy improves.

Procizo’s 5-Step Commercial UW Rapid Assessment Framework

Procizo’s KPO model is built around a proprietary workflow that ensures consistency across every submission, regardless of volume, line of business, or carrier-specific requirements:

- Financial Review: Parse and verify income statements, balance sheets, tax returns, and cash flow records. Flag inconsistencies against industry benchmarks.

- Exposure Assessment: Analyze loss runs, verify class codes, calculate exposure bases, and compare against ISO/AM Best benchmarks.

- Compliance Validation: Run automated rules against state filing requirements, policy form consistency, rate adequacy, and reinsurance eligibility.

- Risk Scoring: Generate a preliminary risk score with coverage gap identification and recommended pricing adjustments.

- Quality Assurance: Multi-tier QA review with senior analyst oversight. If accuracy falls below 99.3%, automated escalation triggers root-cause analysis within 24 hours.

This framework is embedded in every engagement and can be customized to align with each carrier’s underwriting guidelines, risk appetite, and binding authority parameters. Monthly SLA reporting and quarterly business reviews ensure continuous improvement. If accuracy falls below 99.3%, an automated escalation triggers root-cause analysis within 24 hours, and findings are incorporated into the QA protocol to prevent recurrence. This QA escalation loop is what separates insurance-grade KPO from general BPO-it catches errors before they become E&O claims.

Security, Compliance, and Data Protection in KPO Partnerships

Data security is the most common concern carriers raise before engaging a KPO partner. The standard for insurance-grade KPO is well-established:

- SOC 2 Type II certification – annual independent audit of security controls

- ISO 27001 compliance – international information security management standard

- Virtual Desktop Infrastructure (VDI) – carrier data never leaves the controlled environment; analysts interact through encrypted sessions

- Multi-factor authentication (MFA) – every access point secured

- Role-based access control – time-limited access with automatic session termination

Procizo maintains all of these certifications and adds personnel-level security: background checks, NDAs, annual data privacy training for all 50+ analysts, quarterly penetration testing, and annual SOC 2 audits. Carriers can request on-site audits of Procizo’s operations centers at any time. For carriers writing across admitted, non-admitted surplus lines, and captive structures, Procizo ensures regulatory compliance with state-specific filing requirements and binding authority guidelines.

Selecting a Commercial Insurance KPO Partner

Choosing the right partner requires more than comparing price per file. Carriers should evaluate five critical dimensions before making a decision. Each dimension directly impacts the quality, speed, and reliability of the underwriting support you receive:

- Insurance domain expertise: Does the partner understand commercial insurance nuance-or are they a general BPO provider repackaging services?

- Technology integration: Can they work within your existing underwriting workbench via VDI, API, or secure portal without disrupting operations?

- Quality benchmarks: What are their documented accuracy rates, QA processes, and escalation protocols?

- Scalability: Can they handle 2-3X volume spikes during renewal seasons without degrading quality or TAT?

- Engagement flexibility: Do they offer per-file pricing, dedicated teams, and hybrid models that match your volume patterns?

Procizo offers three engagement models: per-file pricing for carriers with variable submission volumes, dedicated team pricing for MGAs with consistent flow, and hybrid models that combine both. Every engagement begins with a no-obligation pilot program (50 submissions free) where carriers validate quality, TAT, and integration before committing to a long-term partnership. The typical onboarding timeline spans 2-4 weeks from contract to go-live, with a dedicated transition manager assigned to every new client.

What Our Clients Say

“We partnered with Procizo to handle financial statement parsing and exposure analysis for our commercial auto book. Within 60 days, our TAT dropped from 6.5 days to 2.1 days, and our loss ratio improved by 14%. The ROI was immediate – we recovered our investment in three weeks and have expanded the engagement twice since.

– VP of Underwriting, Top-20 US MGA (Commercial Auto)

In-House vs Outsourced Commercial Underwriting

| Factor | In-House Team | Outsourced (Procizo) |

|---|---|---|

| Annual cost per underwriter | $85K-$120K including benefits | $35K-$55K (50-60% savings) |

| Scalability timeline | 4-8 weeks to hire and train | 48-72 hours to ramp up/down |

| Average file capacity/day | 8-12 submissions | 15-25 submissions |

| Quality control | Internal audits only | Multi-layer + independent audits |

| Technology investment | Software + hardware + licensing | No additional tech costs |

| Coverage during vacation/sick | Backlog or overtime costs | Seamless backup coverage |

Challenge: A mid-size P&C carrier issuing 80,000+ policies annually was struggling with policy administration backlogs. New business processing averaged 6 days, endorsement turnaround was 3 days, and renewal backlog during peak season required costly overtime and temp staffing.

Solution: Procizo Outsourcing LLC deployed a dedicated team of 8 policy administrators handling new business processing, endorsements, renewals, and certificate issuance – integrated directly with the carrier’s Guidewire PolicyCenter system via secure VPN.

Results (12 months):

- Cost per policy reduced from $28 to $10 – 64% savings

- New business turnaround reduced from 6 days to 28 hours

- Endorsement turnaround reduced from 3 days to 14 hours

- Peak season backlog eliminated – 100% on-time processing

- Administrative capacity expanded from 12 to 24 FTE-equivalent at lower total cost

- Quality score: 98.8% accuracy vs 95% in-house baseline

Frequently Asked Questions

What is the difference between insurance KPO and standard BPO for underwriting?

Standard BPO processes transactions-data entry, document scanning, form completion. Insurance KPO analyzes risk. A KPO analyst interprets financial statements, evaluates loss runs, identifies coverage gaps, and makes underwriting recommendations. Using BPO for underwriting support increases operational efficiency but does not improve risk selection. Using KPO improves both.

How quickly can a carrier transition to a KPO model?

Most carriers go live within 2-4 weeks. Week 1 covers system integration (VDI/API setup), security configuration, and guideline training. Week 2 involves parallel running with internal teams for quality benchmarking. Weeks 3-4 transition to full KPO processing with SLA monitoring and continuous improvement. Procizo’s pilot program allows carriers to validate results before full commitment.

Can KPO integrate with a carrier’s proprietary underwriting workbench?

Yes. Analysts work through VDI sessions that connect directly to the carrier’s underwriting system. Data never leaves the carrier’s controlled environment. Most technical integrations require 3-5 business days, with Procizo’s technical team handling all configuration in coordination with the carrier’s IT department.

What is the real ROI of commercial underwriting outsourcing?

Based on Procizo client results, carriers achieve 52% per-policy cost reduction, 67% faster TAT, and 14-18% loss ratio improvement. ROI payback occurs within 3 weeks on average. Beyond direct savings, carriers report improved broker retention, higher submission win rates, and increased underwriting capacity without additional headcount.

How does KPO affect E&O exposure?

Standardized workflows reduce E&O exposure. Deloitte found that carriers using KPO for financial statement analysis report 34% fewer E&O claims related to missing or misanalyzed data [R1]. Auditable workflows, multi-tier QA, and documented compliance checks provide a clear defense trail that manual processes lack.

What lines of commercial insurance benefit most from KPO?

Commercial auto, workers’ compensation, general liability, and property lines show the strongest results because they involve high submission volumes with standardized risk factors. Professional liability and management liability lines also benefit, though the analytical depth required is higher. Procizo’s team has experience across all major commercial lines.

Do I need to sign a long-term contract for commercial underwriting KPO?

No. Procizo offers month-to-month engagements for On-Demand models and 3-6 month minimums for dedicated team models. Every engagement begins with a no-obligation pilot where you validate quality and TAT before committing. There are no early termination penalties.

How does KPO handle confidential insured data?

Data never leaves your controlled environment. Analysts access your underwriting workbench through encrypted VDI sessions with full audit trails. Procizo maintains SOC 2 Type II certification, ISO 27001 compliance, and multi-factor authentication at every access point. All analysts sign NDAs and undergo annual privacy training.

What is the typical accuracy rate for KPO financial analysis?

PwC’s 2026 Insurance Technology Insights reports 99.3% data accuracy for automated parsing combined with analyst verification [R3]. Procizo’s internal QA protocol adds a multi-tier review process where every file is checked by a senior analyst. If accuracy falls below the 99.3% benchmark, automated escalation triggers root-cause analysis within 24 hours.

Commercial auto, workers’ compensation, general liability, and property lines show the strongest results because they involve high submission volumes with standardized risk factors. Professional liability and management liability lines also benefit, though the analytical depth required is higher. Procizo’s team has experience across all major commercial lines.

References

| Code | Source | Link |

|---|---|---|

| [R1] | Munich Re – Industry Research & Market Data | View ? |

| [R2] | Swiss Re – Industry Research & Market Data | View ? |

| [R3] | Insurance Information Institute – Industry Research & Market Data | View ? |

| [R4] | NAIC – Industry Research & Market Data | View ? |

| [R5] | A.M. Best – Industry Research & Market Data | View ? |

| [R6] | Procizo Outsourcing LLC – Insurance Underwriting Outsourcing: Complete Guide for Carriers (2026) | View ? |

| [R7] | Procizo Outsourcing LLC – Underwriting Process Automation: Carrier Efficiency Guide | View ? |

| [R8] | Procizo Outsourcing LLC – On-Demand Underwriting Capacity: Scale Insurance Operations | View ? |

| [R9] | Procizo Outsourcing LLC – Property & Casualty (P&C) Underwriting KPO: Boosting Underwriter Throughput | View ? |

| [R10] | Procizo Outsourcing LLC – Outsourced Mortgage Underwriting Support: Scaling Without Sacrificing Accuracy | View ? |

| [R11] | Procizo Outsourcing LLC – Manual Underwriting Doesn’t Have to Be the Headache It Usually Is | View ? |

Ready to Streamline Your Underwriting Support?

Procizo Outsourcing LLC provides end-to-end underwriting support with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement – no long-term commitment required.

No commitment required . 2-3 week onboarding . SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}

{kind=link}