- Have Questions? Talk to Us

- info@procizo.com

Lending Business: The Ultimate Playbook for Starting & Scaling

RPO Recruitment Guide 2026: Costs, Models & ROI

April 27, 2026

Commercial Underwriting Outsourcing: Scaling Carrier Profitability

May 18, 2026

Key Takeaways

- Know Your Niche: You must decide strictly between consumer lending and commercial lending before you start.

- Compliance is Everything: State and federal regulations will crush you if you don’t secure the right licenses.

- Tech is King: A powerful Loan Management Software (LMS) is non-negotiable for scaling.

- Risk Management: Your underwriting criteria will determine whether you get rich or go bankrupt.

- Outsource to Scale: Smart lenders offshore their underwriting and collections to radically drop overhead costs.

What is a Lending Business and How Does It Actually Work?

It is all about the spread. You acquire money at a low cost, and lend it out at a higher rate.

People often overcomplicate finance. At its absolute core, a lending business operates on a very simple concept: arbitrage. You find a way to get your hands on a large pool of capital at a relatively low interest rate. Then, you turn around and lend that exact same money to someone else at a higher rate. That difference in the middle? That’s your spread, and that’s how you get wealthy. But to survive, you need to understand the different flavors of lending.

Consumer vs. Commercial Lending

Consumer loans deal with individuals, while commercial loans fund businesses. The risks are totally different.

You have to pick a lane. Consumer lending involves handing cash to regular people. Think personal loans, auto loans, or mortgages. The market is massive, but it is also heavily regulated by the government to protect average citizens from predatory rates. Commercial lending, on the other hand, means you are funding other businesses. Maybe you are helping a startup buy new servers, or funding a real estate developer. The ticket sizes are way bigger, and the regulations are generally looser, but if a business goes bankrupt, you could lose millions in a single afternoon.

Direct Lenders vs. Loan Brokers

Direct lenders risk their own cash. Brokers just play matchmaker and take a fee.

Not everyone who starts a lending business actually uses their own money. If you are a direct lender, you are the one taking the risk. The capital comes from your bank account or your investors. If the borrower defaults, you take the hit. A loan broker operates totally differently. Brokers just connect borrowers with huge banks or private funds. They do all the legwork, close the deal, take a fat commission check, and walk away with zero long-term risk. Both are highly lucrative, but they require totally different skill sets.

Related: Loan Underwriting Process: Complete Guide for Lenders (2026) | Merchant Cash Advance: The Complete Guide for Borrowers and Lenders (2026) | MCA Underwriting: The Complete Guide to Merchant Cash Advance Underwriting Process

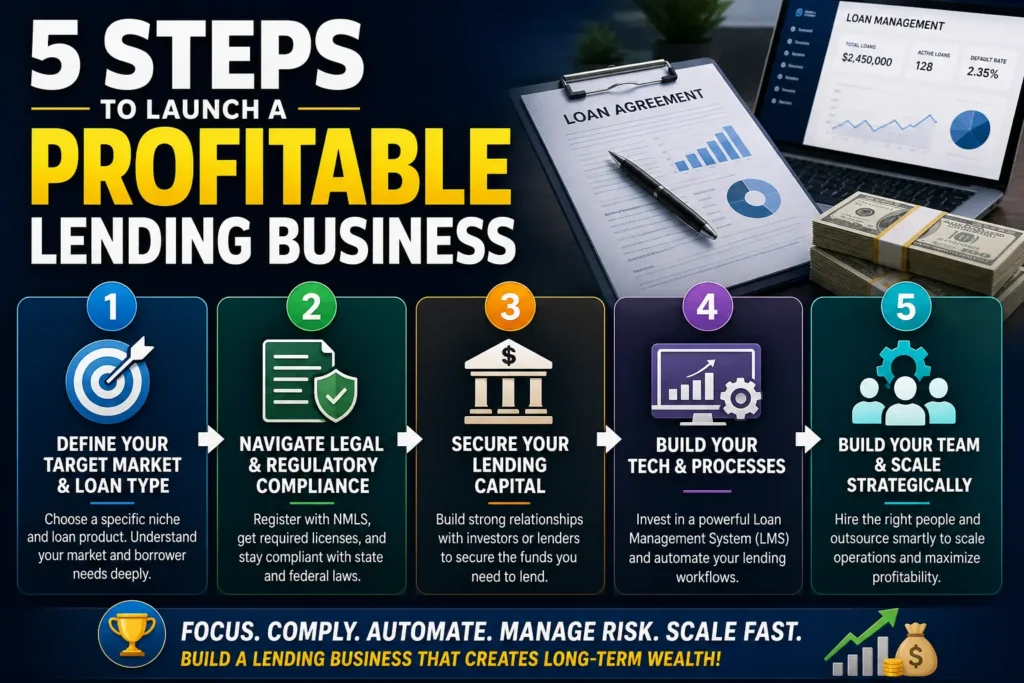

5 Steps to Launch a Profitable Lending Business

You can’t wing this. You need a rock-solid business model, massive compliance, and serious software.

Let’s get down to the actual execution. You can’t just throw up a website and start wiring people cash. That’s a fast track to federal prison. The barrier to entry here is high, which is exactly why the profits are so good. If you want to build a legitimate lending empire, you need to follow a very strict, highly calculated path.

Step 1: Define Your Target Market and Loan Type

Stop trying to be everything to everyone. Pick one highly specific loan product and dominate it.

The worst thing you can do is launch a generic “we lend money company. The big banks will crush you. You need a niche. Maybe you want to focus exclusively on medical practice loans. Maybe you want to fund fix-and-flip real estate investors. By hyper-focusing on one specific industry, you learn exactly how their cash flow works. That makes you way better at predicting who will actually pay you back. Master one tiny corner of the market before you ever try to expand.

Step 2: Navigate Legal and Regulatory Compliance (NMLS)

Get a lawyer immediately. State and federal lending laws are a total minefield.

This is where most people quit. Every single state has its own crazy set of rules regarding interest rate caps, also known as usury laws. If you accidentally charge 1% over the legal limit in California, you are going to get sued into oblivion. Depending on what you are doing, you will likely need to register with the Nationwide Multistate Licensing System (NMLS). Do not try to DIY this. Spend the money to hire a serious financial compliance attorney. It is the cheapest insurance policy you will ever buy.

Step 3: Secure Your Lending Capital

You need two piles of cash: one to keep the lights on, and one to lend out to your clients.

A lending business without money is just a guy with a website. You need serious capital. But you actually need two separate buckets. First, you need operating capital. This pays for your lawyers, your software, and your marketing. Second, you need debt financing. This is the massive pool of money you are going to lend out. Most startups pull this together by pitching high-net-worth individuals, securing warehouse lines of credit from regional banks, or raising a private equity fund.

Step 4: Choose the Right Loan Management Software (LMS)

If you try to track loans on a spreadsheet, your company will collapse. Buy enterprise software.

Do you really want to manually calculate daily interest accruals for 500 different clients? No. You need Loan Management Software. A high-end LMS handles the entire loan origination process. It pulls credit reports automatically, generates the legal contracts, tracks the monthly payments, and automatically sends angry emails when people are late. Yes, the software is expensive. But without it, your operational overhead will explode, and human error will eventually destroy your ledgers.

Step 5: Establish Strict Underwriting Criteria

Underwriting is the heartbeat of your business. Stick to the math and ignore the sob stories.

This is where you actually make or break the business. Underwriting is the process of deciding if someone is too risky to lend to. You need a totally emotionless, mathematical formula. What is their debt-to-income ratio? What collateral are they putting up? If someone begs you for a loan but their credit score is a disaster, you have to say no. The second you start bending your own underwriting rules because you “have a good feeling about a guy, you are digging your own grave.

Scaling Operations: The Role of Outsourcing in Lending

Smart lenders offshore their back-office tasks to scale rapidly without burning through cash.

Here is a secret that the massive financial institutions don’t want you to know. They do not do all the work themselves. As your lending business grows, the sheer amount of paperwork becomes suffocating. Every loan application requires verifying bank statements, checking tax returns, and running compliance checks. If you hire internal staff in New York or London to do this, your payroll will destroy your profit margins.

This is where Business Process Outsourcing (BPO) steps in. Elite lending companies offshore their underwriting support, customer service, and early-stage collections to highly skilled financial teams in places like the Philippines or India. By outsourcing these repetitive tasks, they convert massive fixed salaries into cheap, variable costs. Your expensive domestic team focuses on closing big deals, while the outsourced team handles the heavy lifting in the background. It is the ultimate hack for scaling a financial empire.

Real-World Examples: Successful Lending Business Models

Look at how real startups found a tiny niche and scaled it into millions in revenue.

Theory is great, but let’s look at how this actually works in the real world. You don’t need a billion dollars to start. You just need a smart angle and tight risk management. Here are two examples of lending business models that crushed it.

Example 1: B2B Equipment Financing Startup

A startup ignored consumer loans and focused entirely on helping construction crews buy bulldozers.

A couple of finance guys realized that small construction companies were getting rejected by major banks when they tried to buy used heavy machinery. The big banks thought it was too risky. So, these guys launched a commercial lending company specifically for used construction equipment. Because they understood the exact resale value of a bulldozer, their underwriting was flawless. If a contractor defaulted, they simply repossessed the machine and sold it the next day. By hyper-focusing on one physical asset, they built a $50 million portfolio in three years.

Example 2: Digital Micro-Lending Platform

Lending tiny amounts of money to thousands of people using fully automated software.

A tech founder didn’t want to deal with massive corporate loans. Instead, she built a mobile app that offered $500 emergency loans to gig economy workers (like Uber drivers). The brilliance was in the software. The app automatically scanned the driver’s bank account to verify their weekly income. If the math worked, the loan was approved instantly without a human ever touching it. Because the loans were so small, a few defaults didn’t hurt the bottom line, and the high volume generated insane revenue through origination fees.

Common Mistakes That Destroy Lending Startups

Bad underwriting and ignoring legal compliance will put you out of business incredibly fast.

Lending money is easy. Getting it back is the hard part. The absolute biggest mistake new lenders make is chasing volume over quality. They get excited and start approving terrible loans just to get their capital out the door. Six months later, their default rate skyrockets, and their investors pull their funding. Another massive trap is ignoring state usury laws. If you try to sneak hidden fees into a consumer loan to boost your yield, state regulators will eventually catch you. They will freeze your assets and fine you into oblivion. Play by the rules, stick strictly to your underwriting math, and never lend money you can’t afford to lose.

Best Practices for Managing Risk and Defaults

Have a ruthless collections strategy and demand hard collateral whenever possible.

You have to accept reality: some people are going to take your money and refuse to pay it back. It is just part of the game. Your job is to make sure those losses are already baked into your business model. First, demand hard collateral whenever you can. If you are lending to a business, put a lien on their real estate or their expensive equipment. Second, act immediately when someone misses a payment. Do not wait thirty days. If they are 48 hours late, your outsourced collections team needs to be blowing up their phone. The longer you wait to collect, the lower your chances of ever seeing that money again.

FAQ: Starting and Running a Lending Business

The blunt answers to your biggest questions about money, risk, and massive profitability.

How much money do you need to start a lending business?

It varies, but you need enough to cover expensive legal fees before you ever make a loan.

Startup costs vary wildly. A small micro-lending firm might launch with $100,000, while a robust commercial lending company needs millions in debt financing just to begin underwriting. At a minimum, expect to spend heavily on legal compliance and loan management software before you even open your doors.

Is the lending business profitable?

Yes, but only if you are obsessed with controlling your default rates.

Yes, incredibly so. However, profitability entirely depends on your underwriting criteria. If you control your default rates and keep operational overhead low, the margins are massive. If you hand out cash to risky borrowers, you will go bankrupt within a year.

How do lending companies make money?

They make their cash on the interest rate spread and a mountain of origination fees.

They make money through interest rate spreads, origination fees, late payment penalties, and servicing fees. The core goal is lending out money at a higher interest rate than the cost of acquiring that capital from your investors or banks.

2026 Lending Business Models Comparison

| Feature | Traditional Lender | Tech-Enabled Lender | Outsourced-Operations Lender |

|---|---|---|---|

| In-house underwriting | Yes (full team) | Partial (hybrid) | Fully outsourced |

| Operating cost per loan | $850-$1,200 | $550-$800 | $350-$550 |

| Processing time | 7-14 days | 3-7 days | 2-4 days |

| Scalability | Limited by headcount | Moderate | Instant elasticity |

| Technology infrastructure | Legacy systems | Modern tech stack | Leverage partner tech |

| Focus on core business | Diluted by ops management | Improved | Maximum |

Challenge: A growing business was facing operational bottlenecks in their core processes. Manual workflows, limited team capacity, and rising labor costs were constraining growth. In-house processing was slow, error-prone, and difficult to scale during peak periods.

Solution: Procizo Outsourcing LLC analyzed the client’s workflows and deployed a dedicated team with the right skill mix. The team was integrated into the client’s existing systems and processes within 2-3 weeks, operating as a seamless extension of their operations.

Results (6 months):

- Operational costs reduced by 50-65% across outsourced functions

- Processing turnaround improved by 60-85% depending on function

- Team capacity scaled 2-3x without additional management overhead

- Accuracy and quality improved through structured QA protocols

- Internal teams refocused on core strategic activities

- Client reported significant improvement in customer satisfaction scores

Frequently Asked Questions

What is a lending business in 2026?

A lending business in 2026 is any organization that provides capital to borrowers – including traditional banks, credit unions, online lenders, MCA funders, and peer-to-peer lending platforms. The 2026 lending landscape is characterized by AI-driven underwriting, embedded finance, and highly competitive rates.

How has lending changed in 2026?

Key changes include AI-powered credit decisioning reducing approval times to minutes, open banking APIs providing real-time cash flow data, embedded lending [R3] integrated into e-commerce and POS systems, and increased regulatory scrutiny on alternative lending products.

What are the most profitable lending segments in 2026?

Small business lending, merchant cash advance (MCA), equipment financing, invoice factoring, and buy-now-pay-later (BNPL) continue to offer strong margins. MCA remains profitable due to its flexible structure and high approval rates despite regulatory attention.

Do lenders in 2026 still outsource underwriting?

Yes – more than ever. Outsourcing underwriting gives lenders access to experienced professionals without fixed overhead, enables 24/7 processing across time zones, and provides instant scalability during volume spikes. Procizo Outsourcing LLC provides underwriting support for MCA, mortgage, and commercial lenders.

What technology do modern lenders use?

AI underwriting engines, automated decisioning systems, digital verification tools (bank statement analysis, income verification APIs), cloud-based LOS platforms, and blockchain for secure document management. However, human underwriters remain essential for complex cases and relationship-based lending.

Is MCA lending still viable in 2026?

Yes. MCA remains a $40+ billion industry. Regulation is increasing (especially at the state level), which favors compliant funders. MCA brokers and funders who partner with experienced underwriting support providers like Procizo are best positioned to navigate the regulatory landscape.

How do I start a lending business in 2026?

Define your niche (MCA, SMB loans, invoice factoring, etc.), secure funding from investors or lenders, obtain necessary licenses (varies by state), build technology infrastructure or partner with existing platforms, develop underwriting criteria, and establish risk management processes.

What are the biggest risks for lenders in 2026?

Credit risk (borrower default), regulatory compliance risk (state and federal lending laws), interest rate risk, operational risk (processing errors), and competition risk (fintech disruption). Mitigation requires robust underwriting, legal compliance, and diversified funding sources.

How does Procizo help lending businesses?

Procizo Outsourcing LLC provides end-to-end underwriting support for MCA funders, commercial lenders, and mortgage companies – including bank statement analysis, risk scoring, compliance verification, condition clearing, and file audits. Visit {https://procizo.com/our-services/} for details.

References

| Code | Source | Link |

|---|---|---|

| [R1] | IBISWorld – Industry Research & Market Data | View ? |

| [R2] | Dun & Bradstreet – Industry Research & Market Data | View ? |

| [R3] | Experian – Industry Research & Market Data | View ? |

| [R4] | Federal Reserve – Industry Research & Market Data | View ? |

| [R5] | SBA – Industry Research & Market Data | View ? |

| [R6] | Procizo Outsourcing LLC – Loan Underwriting Process: Complete Guide for Lenders (2026) | View ? |

| [R7] | Procizo Outsourcing LLC – Merchant Cash Advance: The Complete Guide for Borrowers and Lenders (2026) | View ? |

| [R8] | Procizo Outsourcing LLC – MCA Underwriting: The Complete Guide to Merchant Cash Advance Underwriting Process | View ? |

| [R9] | Procizo Outsourcing LLC – What Is MCA Underwriting? The Complete Process for Funders (2026) | View ? |

| [R10] | Procizo Outsourcing LLC – What Is Underwriting? Complete Guide for Business Lending (2026) | View ? |

| [R11] | Procizo Outsourcing LLC – The Complete Guide to MCA Underwriting Outsourcing (2026) | View ? |

Ready to Streamline Your Professional Outsourcing Solutions?

Procizo Outsourcing LLC provides end-to-end professional outsourcing solutions with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement – no long-term commitment required.

No commitment required . 2-3 week onboarding . SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}

{kind=link}