- Have Questions? Talk to Us

- info@procizo.com

What MCA Tasks Should You Outsource? (2026 Guide)

Why MCA Businesses Need Outsourcing — Cut Costs by 60%

January 31, 2025

How to Find the Best Outsourcing Company for MCA (2026 Guide)

February 10, 2025

Quick Answer

Which MCA tasks should you outsource? The most outsourced MCA tasks are: underwriting and risk assessment, bank statement scrubbing, CRM and pipeline management, lead pre-qualification, deal pricing and structuring, virtual assistant support, and back-office document processing. By outsourcing these, MCA funders and brokers cut operational costs by 40–60%, reduce turnaround from days to 24 hours, and eliminate the time and expense of hiring and training in-house teams [R1].

About the Author

Shubham Pathak — Content Writer, Procizo Outsourcing LLC. With 3+ years covering MCA and alternative lending operations, Shubham helps US-based funders evaluate outsourcing strategies that reduce costs and accelerate deal flow.

1. Why Outsource MCA Tasks at All?

The Merchant Cash Advance industry runs on speed. Every hour between application and funding risks losing the deal to a faster competitor. Yet most MCA companies operate with small in-house teams that hit capacity limits fast.

According to industry data, an in-house underwriter costs $65,000–$85,000 per year including benefits [R1]. When deal volume fluctuates — heavy in Q4 and tax season, slower in mid-summer — you either pay for idle capacity or miss deals during peak periods. Outsourcing solves both problems.

The U.S. MCA market has grown from $19.7 billion in 2024 to an estimated $32 billion by 2032 [R2]. As volume increases, the companies that scale their operations without scaling their payroll win. The rest get bottlenecked.

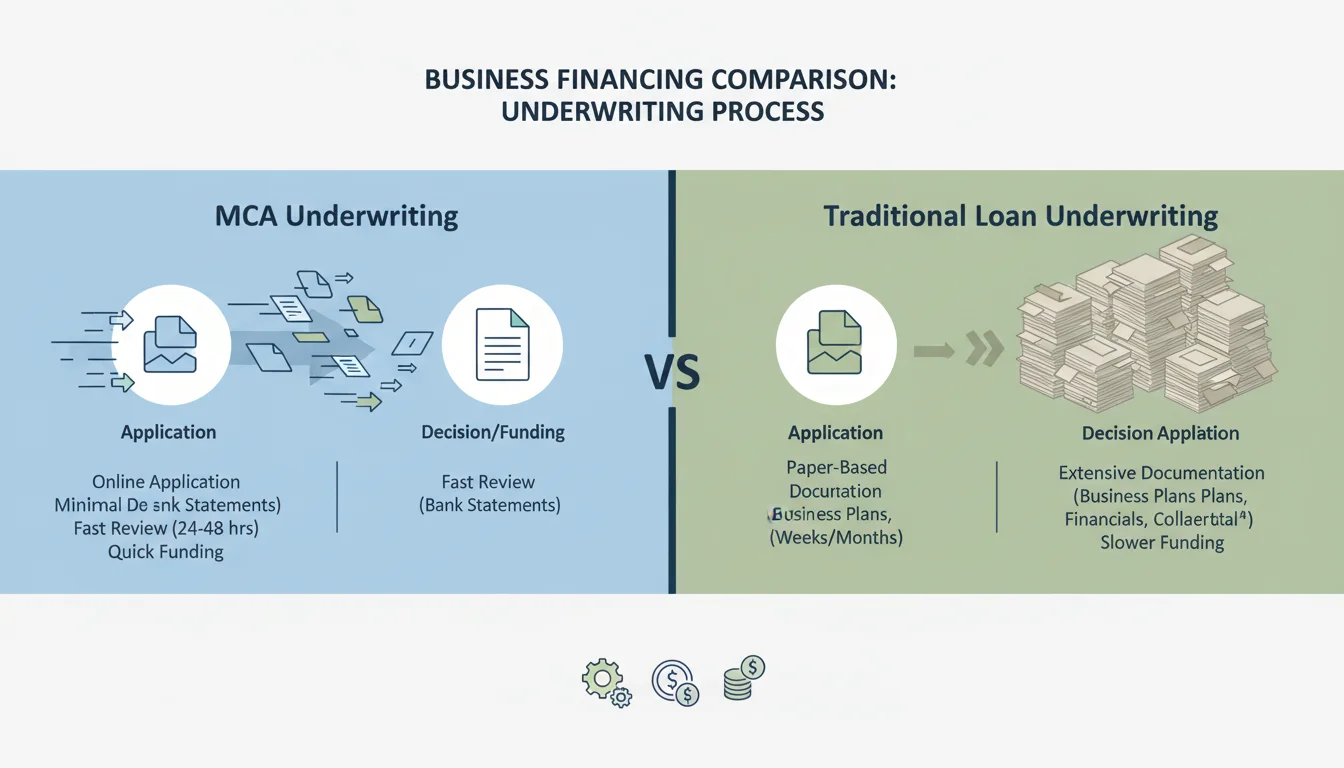

2. Task #1: MCA Underwriting and Risk Assessment

What it involves: Application intake, bank statement analysis, cash flow evaluation, NSF detection, risk scoring, factor rate pricing, and funding recommendation.

Why outsource: Underwriting is the most time-intensive MCA task. A single deal can require reviewing 3–6 months of bank statements, cross-referencing deposit patterns against merchant-provided revenue numbers, flagging NSF items, and calculating repayment capacity.

An experienced outsourced underwriter completes this in 2–4 hours per deal — versus 6–8 hours for an in-house team without dedicated statement processing tools [R1]. Partners proficient in HeronData, Ocrolus, and MoneyThumb process standard files in under 24 hours with 99%+ accuracy.

3. Task #2: Bank Statement Scrubbing

What it involves: Depositing and cleaning merchant bank statements — extracting deposit amounts, flagging negative days, calculating average daily and monthly revenue, detecting NSF frequency, and identifying cash flow patterns.

Why outsource: Bank statement scrubbing is the most commonly outsourced MCA task for one reason: it is repetitive, data-intensive, and directly impacts funding decisions. A single scrubbing error — missing an NSF flag, misreading a deposit — can lead to a bad funding decision.

Tools like HeronData and Ocrolus automate parts of the process, but human review remains critical for nuance: distinguishing a legitimate deposit from a transfer, identifying seasonal revenue dips, and catching obscured NSF entries [R3]. Dedicated scrubbing teams in outsourcing firms develop this judgment through volume — processing hundreds of statements per week versus an in-house team seeing a few dozen.

4. Task #3: CRM and Pipeline Management

What it involves: Deal tracking across stages (lead → submission → underwriting → funding → renewal), broker communication, funder portal submissions, email management, commission tracking.

Why outsource: For brokers managing multiple funders and hundreds of active deals, CRM management becomes a full-time operational role. Outsourcing partners handle daily updates across Salesforce, HubSpot, Zoho, and LendSaas — logging every broker call, every submission date, every funding status change [R1].

This keeps your pipeline real-time without a dedicated in-house CRM manager. The best partners also handle multi-funder portal submissions, ensuring each lender receives deal packages in their required format.

5. Task #4: Lead Pre-Qualification

What it involves: Initial merchant screening — reviewing application completeness, requesting missing documents, verifying basic eligibility criteria before the file reaches underwriting.

Why outsource: Pre-qualification is low-complexity but high-volume. A pre-qual team can screen 20–50 leads per day, rejecting incomplete applications and collecting missing documents before they hit your underwriter’s desk. This ensures your underwriting team only works on fundable deals [R4].

Most MCA companies waste 30–40% of underwriting time on incomplete or unqualified files. Pre-qualification outsourcing eliminates this waste.

6. Task #5: Pricing and Deal Structuring

What it involves: Factor rate calculation based on risk grade, affordability analysis, renewal structuring, payback amount determination.

Why outsource: Pricing is formula-driven but requires market awareness. An outsourced pricing team applies consistent factor rates across deals based on your guidelines — no emotional pricing, no inconsistent offers to similar merchants. They also handle renewal pricing, which requires reviewing the merchant’s payment history and current cash flow data [R1].

7. Task #6: Virtual Assistant Support

What it involves: Email management, calendar scheduling, merchant follow-ups, document collection, broker communication, data entry.

Why outsource: These administrative tasks consume 15–20 hours per week per broker but require no specialized underwriting knowledge. A virtual assistant handles merchant calls (“When will my deal fund?”), collects signed documents, follows up on outstanding stipulations, and keeps the deal pipeline moving [R4].

8. Task #7: Back-Office Document Processing

What it involves: Document verification, file organization, compliance documentation, deal file preparation, deliverable packaging for funders.

Why outsource: Every funded deal generates a documentation trail — signed contracts, funding confirmations, ACH authorization forms, UCC filings. Managing this in-house is tedious and error-prone. Outsourcing partners maintain organized, audit-ready deal files that satisfy compliance requirements [R5]. With CFPB Section 1071 data collection requirements taking effect in 2026, organized documentation is no longer optional [R2].

9. Which MCA Tasks Should You NOT Outsource?

Not every task belongs with an external partner. Keep these in-house:

- Final funding approval: The decision to fund or decline should always rest with your internal team. The outsourcing partner recommends — you decide.

- Broker relationship management: Building and maintaining broker relationships requires direct, personal communication that cannot be delegated.

- Strategic decisions: Underwriting policy changes, risk tolerance adjustments, new product development — these require internal leadership.

- Compliance oversight: While outsourcing partners can prepare documentation, final compliance sign-off should be internal.

10. How to Decide What to Outsource: A Framework

Use this framework to evaluate each task:

- Is the task repetitive and rule-based? Yes → outsource. No → evaluate further.

- Does it require MCA-specific expertise? Yes → outsource to a specialist. No → outsource to a generalist BPO.

- Does it contain sensitive strategic decisions? Yes → keep in-house.

- Does it directly generate revenue? Yes → keep in-house or co-manage with oversight.

11. MCA Outsourcing Pricing by Task

| Task | Typical Pricing | Best For |

|---|---|---|

| MCA Underwriting | $20–$50 per file | Full-cycle underwriting |

| Bank Statement Scrubbing | $10–$25 per statement set | High-volume document processing |

| CRM Management | $1,500–$4,000/month | Dedicated pipeline support |

| Lead Pre-Qualification | $8–$15 per screened lead | Incomplete file filtering |

| Virtual Assistant | $12–$20/hour | Administrative overflow |

| Back-Office Processing | $1,000–$3,000/month | Document management |

Most providers offer blended pricing — combine tasks for better rates. Always request a pilot program before committing [R5].

Frequently Asked Questions

What is the most commonly outsourced MCA task? Bank statement scrubbing is the most commonly outsourced MCA task because it is repetitive, data-intensive, and directly impacts funding decisions.

How much does MCA task outsourcing cost? Costs range from $8–$15 per lead for pre-qualification, $10–$25 per statement set for scrubbing, $20–$50 per file for underwriting, $12–$20 per hour for virtual assistants, and $1,000–$4,000 per month for dedicated support [R5].

Can I outsource MCA underwriting decisions? Final funding decisions should stay in-house. An outsourcing partner recommends — you approve. Strategic control remains with your team.

Is my merchant data safe with an outsourcing partner? Yes, when you work with a SOC 2 compliant partner. Always verify certifications, encrypted data handling, and NDA coverage before sharing merchant data.

Should I outsource all MCA tasks together? Many funders start with one task (bank statement scrubbing) and expand as trust builds. Most full-outsourcing relationships begin with scrubbing and add underwriting → CRM → VA support over 3–6 months.

Ready to Start Outsourcing MCA Tasks?

Procizo specializes in MCA underwriting, bank statement scrubbing, CRM management, and VA support for US-based funders and brokers. Our teams process standard files in under 24 hours with 99%+ accuracy. Contact us for a free pilot — try a single task before committing.

References

[R1] Industry benchmarks — MCA underwriting task cost analysis and operational data (2025–2026).

[R2] Fusion CX — Merchant Cash Advance BPO Market Analysis (2026). Market growth data and regulatory overview.

[R3] HeronData/Glossary — Bank Statement Scrubbing definition and process. https://www.herondata.io/glossary/bank-statement-scrubbing

[R4] Target Underwriting Solutions — MCA Outsourcing Services. https://www.targetunderwriting.com

[R5] Procizo — MCA Outsourcing Service Provider pricing data. https://procizo.com/mca-outsourcing-service-provider-in-usa/

{kind=link}

{kind=link}

{kind=link}