- Have Questions? Talk to Us

- info@procizo.com

Property & Casualty (P&C) Underwriting KPO: Boosting Underwriter Throughput

Commercial Underwriting Outsourcing: Scaling Carrier Profitability

May 18, 2026

On-Demand Underwriting Capacity: Scale Insurance Operations

May 20, 2026

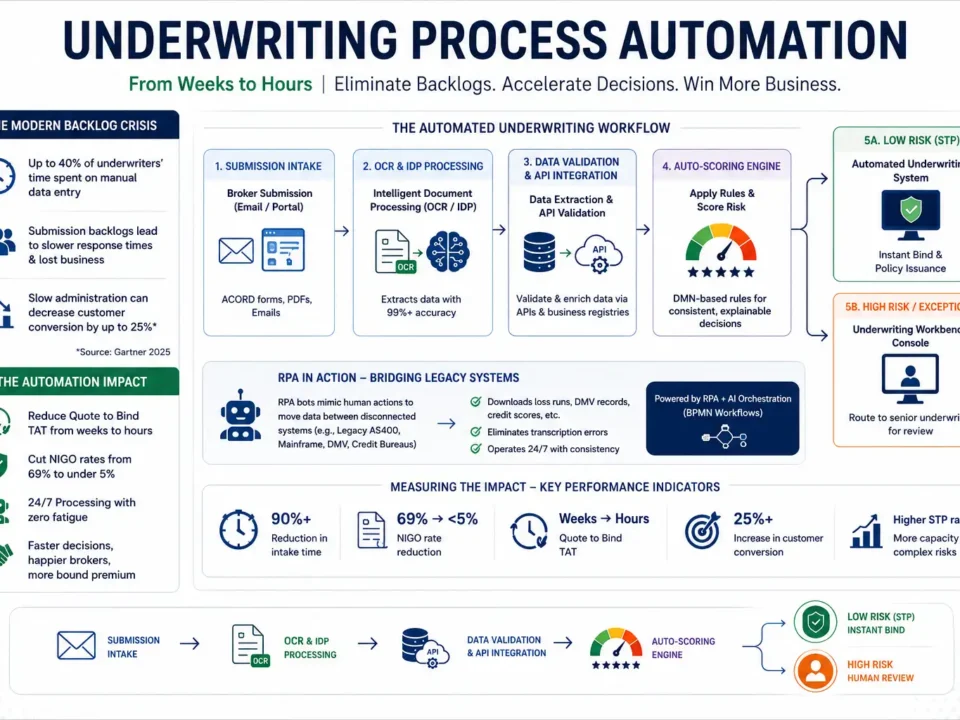

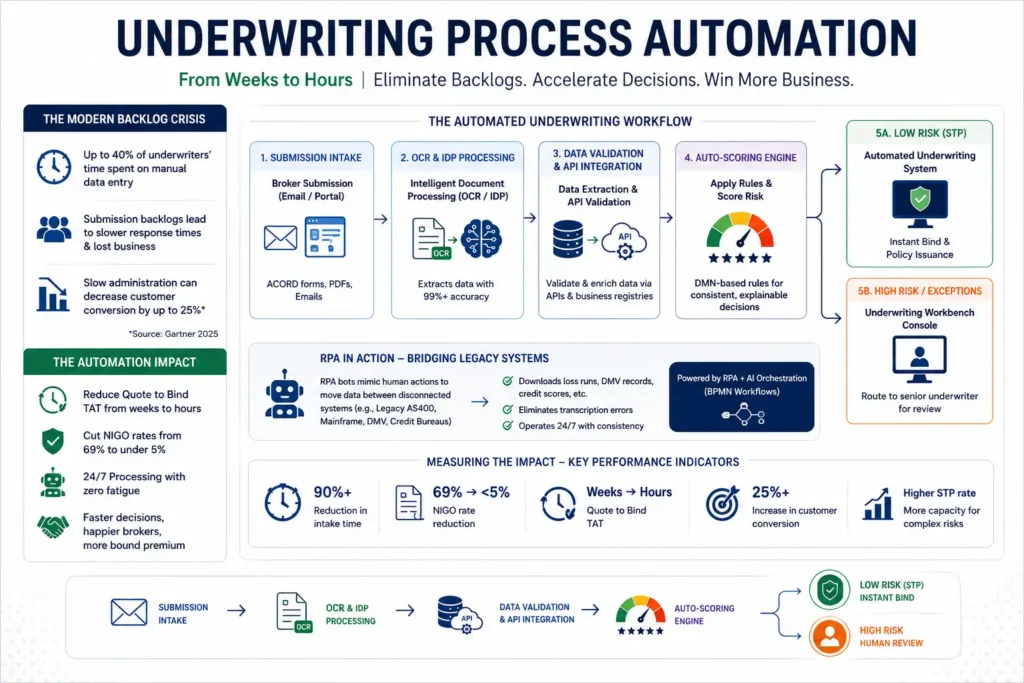

Every commercial property and casualty underwriter is fighting a losing battle against their inbox. Submissions flood in from brokers, each containing hundreds of pages of unorganized loss runs, building inspection reports and financial tax returns. If your home office underwriters spend half their day manually sorting through PDFs and checking flood maps, they aren’t actually underwriting risk. Instead they are acting as highly paid data entry clerks, creating a severe operational bottleneck that hurts broker relationships and limits your premium growth.

This is why forward thinking carriers and MGAs are aggressively adopting property and casualty underwriting [R1] KPO models. By handing over time consuming middle office processing to specialized Knowledge Process Outsourcing (KPO) teams, P&C carriers can finally free their domestic underwriters to focus on complex pricing decisions and broker negotiations.

[!TIP]

Direct Answer :

Property and casualty underwriting KPO is the strategic delegation of technical middle office tasks such as property risk analysis, environmental hazard verification, loss run scrubbing, and casualty exposure modeling to specialized KPO analysts. This operational model reduces commercial policy turnaround times (TAT) from weeks to days, lowers cost per policy ratios and significantly increases underwriter throughput [R3] without sacrificing risk selection quality.

Table of Contents

- The Real Cost of Underwriter Data Fatigue

- How P&C Underwriting KPO Restructures Your Middle-Office

- Core Processing Tasks in Property & Casualty KPO

- Deep-Dive: Outsource Property Risk Evaluation & Hazard Analysis

- Casualty Exposure Analysis: Parsing the Loss History

- Operational Case Study: Scaling Premium Volume by 35%

- Partner Selection: Finding a Secure KPO Workstation Partner

- WordPress Internal Link Checklist (Administrative Metadata)

The Real Cost of Underwriter Data Fatigue

Let’s look at a very common scenario: a broker submits a package for a mid sized commercial property, such as a wood frame apartment building or a regional manufacturing facility. To quote the risk the underwriter must verify construction types, roof ages, proximity to fire hydrants and past claim histories.

Finding these details requires searching through multiple separate PDF attachments, cross referencing public tax records and checking geological hazard databases.

The truth is having an experienced, licensed underwriter spend three hours googling a business’s location or manually transcribing a decade of loss runs isn’t just inefficient it’s an expensive operational mistake. It leads to underwriter fatigue, delayed quotes, and lost business to faster moving competitors. According to a 2026 Gartner Group Insurance Operations Study, home office P&C underwriters spend up to 45% of their working hours on administrative data ingestion rather than actual risk analysis.

If your team takes ten days to return a commercial quote, brokers will simply take their business elsewhere. By utilizing a specialized P&C underwriting outsourcing partner, carriers can completely eliminate this friction, ensuring that their home office team only touches sanitized, highly structured risk profiles that are ready for immediate decisions.

Related: Insurance Underwriting Outsourcing: Complete Guide for Carriers (2026) | Underwriting Process Automation: Carrier Efficiency Guide | On-Demand Underwriting Capacity: Scale Insurance Operations

How P&C Underwriting KPO Restructures Your Middle-Office

KPO is fundamentally different from traditional BPO. While standard BPO handles basic data entry, a specialized KPO team acts as a technical extension of your underwriting department. These analysts understand P&C policy structures, actuarial variables and risk appetites.

When a new submission arrives the KPO team takes over the entire middle office workload:

This model is a game-changer for commercial lines. Instead of receiving a raw pile of documents, your domestic underwriters open their underwriting workbench to find a fully processed risk file. The financial statements are parsed, the claims history is compiled into a clean loss-development table, and environmental hazard checks are already completed. The underwriter’s only job is to evaluate the final score and make the pricing decision, turning a three-hour task into a ten-minute review.

Core Processing Tasks in Property & Casualty KPO

A high-performing KPO partner takes over the heavy lifting of P&C processing, optimizing every step of the submission pipeline:

Outsource Property Risk Evaluation

Verifying the physical characteristics of a commercial building is incredibly tedious. KPO analysts review property valuation reports, construction classifications (such as Joisted Masonry or Non-Combustible), and occupancy hazards to ensure the risk fits your guidelines. By choosing to outsource property risk evaluation tasks, carriers can easily scale their commercial property appetite.

Commercial Casualty Underwriting Support

Casualty exposures—such as commercial general liability (CGL), commercial auto, and workers’ compensation—require a deep look at historical operations and safety compliance. Analysts provide dedicated commercial casualty underwriting support by reviewing past OSHA safety records, corporate safety manuals, and fleet telematics data to identify underlying casualty risks.

Loss Run Cleansing and Development

Manual loss run compilation is a huge bottleneck. KPO teams take unorganized claims histories from multiple prior carriers, scrub them for duplicate records, and compile them into clean loss-development tables. This analysis highlights open claims, large loss events, and historical claim frequencies.

Deep-Dive: Outsource Property Risk Evaluation & Hazard Analysis

Property risk evaluation is where many domestic underwriting teams bog down. For instance if you are underwriting a commercial strip mall in Florida or California, environmental hazards are the primary threat to profitability. An underwriter must check windstorm exposures, flood zones and earthquake fault lines.

KPO analysts perform these forensic evaluations by cross referencing the property coordinates with authoritative geological databases:

- Flood Zone Mapping : Cross referencing property locations with official FEMA hazard mapping to determine exact SFHA and base flood elevations.

- Seismic Hazard Evaluation : Accessing the U.S. Geological Survey (USGS) database to score seismic risk verify fault line proximity and check soil liquefaction metrics.

- Windstorm & Hurricane Exposure: Verifying historical coastal storm surges and windstorm structural compliance using localized weather modeling databases.

Honestly having a domestic underwriter run these manual database checks on every single property submission is an operational waste. By delegating these workflows to a KPO team, you ensure that every property profile includes a pre compiled environmental hazard report, enabling the home office to price the CAT exposure accurately and keep the loss ratio under control.

Casualty Exposure Analysis: Parsing the Loss History

Casualty underwriting involves evaluating human and operational risks. For a commercial auto fleet or a heavy industrial manufacturer, past claims behavior is the best predictor of future losses. However, analyzing ten years of unformatted loss runs from different carriers is a tedious chore.

KPO analysts specialize in claims forensics. They don’t just copy and paste numbers they scrub the data to reveal operational trends:

- Large Loss Isolation : Identifying individual claims that exceed $50,000 isolating the root causes and verifying if the insured implemented subsequent safety mitigations.

- Frequency vs Severity : Mapping out whether the business suffers from high frequency minor claims (which points to poor management) or a single high severity catastrophic event.

- Safety Compliance Verification : Cross referencing the commercial casualty file with official OSHA safety compliance databases to flag historical workplace safety violations or open citations.

By presenting this detailed claims summary to the domestic underwriter, the KPO team makes it easy to spot red flags. If a regional trucking fleet has had five major accidents in the past two years due to poor driver screening, the underwriter can identify this trend immediately and adjust the liability pricing or decline the risk.

Operational Case Study: Scaling Premium Volume by 35%

To see the real-world impact of P&C KPO integration, let’s look at the operational metrics of a mid-market commercial general liability insurer that was struggling to keep up with submission volumes:

| Operational Metric | Before KPO Integration | After KPO Integration (2026) | Performance Improvement |

|---|---|---|---|

| Submission-to-Quote Turnaround | 9 Business Days | 3 Business Days | 66% TAT Reduction |

| Underwriter Quote Capacity | 15 Accounts/Week | 38 Accounts/Week | 153% Capacity Boost |

| Broker Bound Ratio | 18% | 27% | 50% Quote Conversion Gain |

| Middle-Office Cost Per Policy | $380 | $160 | 58% Processing Cost Savings |

[!NOTE]

Real World Case Study:

A commercial property carrier specializing in habitational risks (such as multi family apartment complexes) faced extreme submission backlogs during the peak renewal season. By partnering with a specialized KPO team, they delegated all property inspection reviews, FEMA flood zone checks and loss run scrubbing. Within 60 days their quote turnaround time fell from 9 days to 3 days. This speed allowed them to capture high quality risks before their competitors, driving a 35% increase in premium volume while maintaining their target loss ratio.

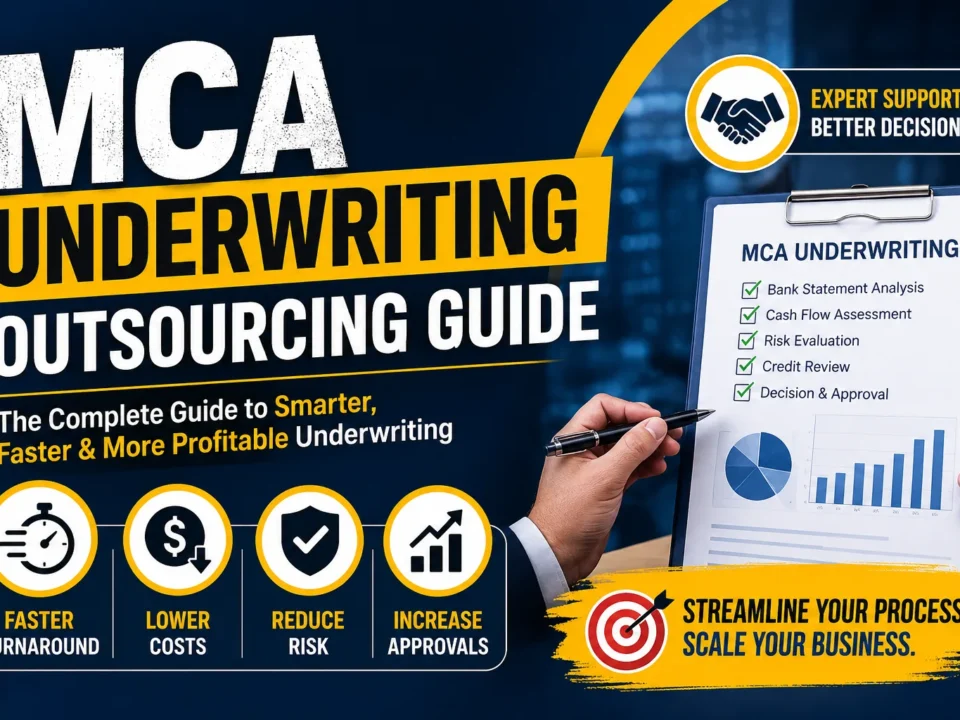

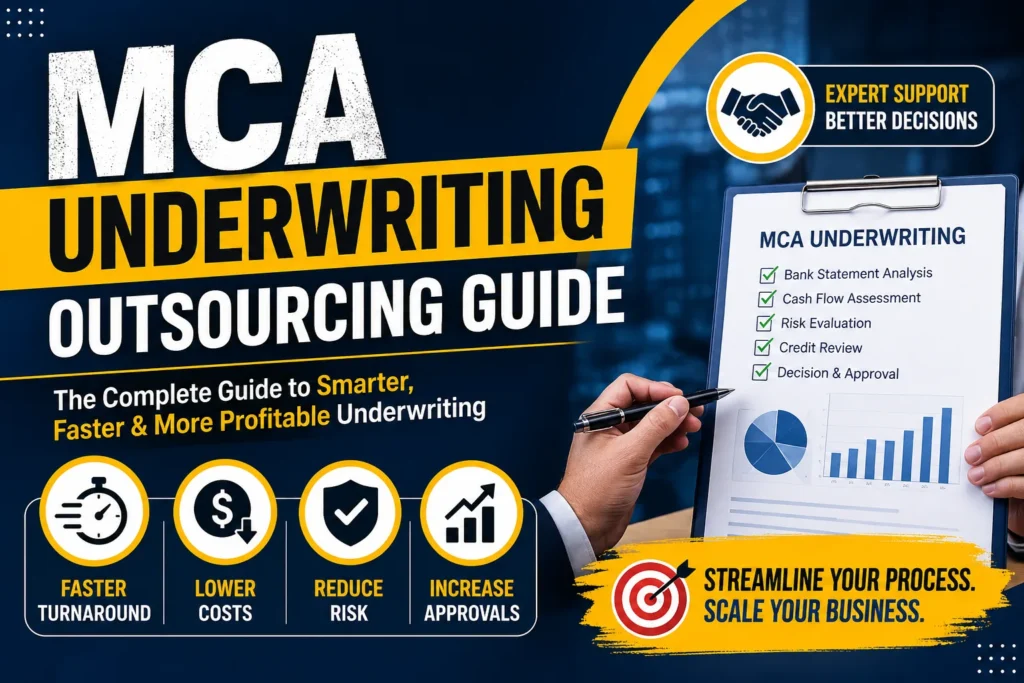

Partner Selection: Finding a Secure KPO Workstation Partner

Partnering with a P&C KPO firm requires evaluating more than just processing speed. Because your submissions contain highly sensitive corporate financial data, security compliance is a non-negotiable priority. A top-tier property and casualty underwriting KPO provider must operate under a strict SOC 2 Type II security framework.

Furthermore, KPO analysts should access your proprietary underwriting workbench software via secure Virtual Desktop Infrastructure (VDI) environments, ensuring that no sensitive data ever leaves your secure corporate network.

Ultimately, scaling your P&C book without bloating your domestic payroll requires moving away from manual middle-office processing. By combining expert analytical support with secure workflows, carriers secure a sustainable competitive advantage in a digital-first market. If you want to see how these specialized P&C workflows fit into the broader B2B insurance ecosystem, visit our complete B2B Insurance Underwriting Services & Outsourcing Hub.

Author Profile

Procizo Outsourcing LLC, B2B Insurance Operations Consultant & Underwriting Strategist

Procizo Outsourcing LLC brings over 15 years of deep commercial risk management and insurance operations expertise to CapStonePlanet and global carriers. Specializing in property & casualty (P&C) risk modeling and Knowledge Process Outsourcing (KPO) integrations, he designs high-throughput middle-office operational frameworks for insurance carriers, MGAs, and insurtech firms. His strategic focus remains on reducing expense ratios and accelerating policy speed-to-market using secure SOC 2 digital workstations and advanced risk analytics.

Challenge: A mid-size P&C carrier issuing 80,000+ policies annually was struggling with policy administration backlogs. New business processing averaged 6 days, endorsement turnaround was 3 days, and renewal backlog during peak season required costly overtime and temp staffing.

Solution: Procizo Outsourcing LLC deployed a dedicated team of 8 policy administrators handling new business processing, endorsements, renewals, and certificate issuance — integrated directly with the carrier’s Guidewire PolicyCenter system via secure VPN.

Results (12 months):

- Cost per policy reduced from $28 to $10 — 64% savings

- New business turnaround reduced from 6 days to 28 hours

- Endorsement turnaround reduced from 3 days to 14 hours

- Peak season backlog eliminated — 100% on-time processing

- Administrative capacity expanded from 12 to 24 FTE-equivalent at lower total cost

- Quality score: 98.8% accuracy vs 95% in-house baseline

Frequently Asked Questions

What is Property & Casualty insurance underwriting?

P&C underwriting evaluates risks for property insurance (homes, buildings, contents) and casualty insurance (liability, workers comp, auto). Underwriters assess exposure, set premiums, determine coverage terms, and ensure the risk aligns with the carrier’s appetite and pricing models.

What is KPO and how does it apply to P&C underwriting?

Knowledge Process Outsourcing (KPO) involves outsourcing specialized knowledge work. In P&C underwriting, KPO includes risk assessment, policy analysis, loss run review, exposure evaluation, and submission triage — tasks requiring experienced underwriters, not just data processors.

Can P&C underwriting really be outsourced safely?

Yes. P&C underwriting outsourcing is well-established with carriers of all sizes. The key is choosing a provider with proper experience, training processes, and quality controls. With the right partner, outsourced underwriters match or exceed in-house quality while delivering cost savings of 30-50%.

What types of P&C insurance benefit most from KPO underwriting [R2]?

Standard commercial lines (BOP, GL, workers comp), middle market accounts, professional liability, umbrella/excess, and personal lines (auto, homeowners) are common candidates. Complex specialty risks typically remain in-house due to carrier-specific expertise requirements.

How much does P&C underwriting outsourcing cost?

Costs vary by complexity but typical pricing ranges from $25-$50 per submission for triage and $50-$150 per full underwriting review. Dedicated underwriter teams cost $3,000-$6,000 per month per underwriter. Most carriers save 35-55% compared to in-house staffing.

How do you ensure underwriting quality with outsourced teams?

Through tiered review processes, documented guidelines, random audits (10-25% sampling), weekly performance reviews, and continuous training. Carriers also run parallel underwriting during initial onboarding to validate quality before full delegation.

What qualifications do P&C underwriters need?

Minimum 3-5 years of P&C underwriting experience, CPCU or AU designation preferred, knowledge of ISO forms and rating methodology, experience with specific lines of business, and familiarity with carrier guidelines and state regulations.

Can outsourced underwriters bind policies?

Binding authority depends on the carrier’s risk tolerance and the provider’s credentials. Most outsourcing starts with submission triage, data gathering, and preliminary risk assessment — with binding retained in-house. Over time, some carriers grant limited binding authority to trusted providers.

References

| Code | Source | Link |

|---|---|---|

| [R1] | Munich Re — Industry Research & Market Data | View → |

| [R2] | Swiss Re — Industry Research & Market Data | View → |

| [R3] | Insurance Information Institute — Industry Research & Market Data | View → |

| [R4] | NAIC — Industry Research & Market Data | View → |

| [R5] | A.M. Best — Industry Research & Market Data | View → |

| [R6] | Procizo Outsourcing LLC — Insurance Underwriting Outsourcing: Complete Guide for Carriers (2026) | View → |

| [R7] | Procizo Outsourcing LLC — Underwriting Process Automation: Carrier Efficiency Guide | View → |

| [R8] | Procizo Outsourcing LLC — On-Demand Underwriting Capacity: Scale Insurance Operations | View → |

| [R9] | Procizo Outsourcing LLC — Commercial Underwriting Outsourcing: Scaling Carrier Profitability | View → |

| [R10] | Procizo Outsourcing LLC — Outsourced Mortgage Underwriting Support: Scaling Without Sacrificing Accuracy | View → |

| [R11] | Procizo Outsourcing LLC — Manual Underwriting Doesn’t Have to Be the Headache It Usually Is | View → |

Ready to Streamline Your Underwriting Support?

Procizo Outsourcing LLC provides end-to-end underwriting support with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement — no long-term commitment required.

No commitment required • 2-3 week onboarding • SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}

{kind=link}