- Have Questions? Talk to Us

- info@procizo.com

5 Reasons MCA Companies Should Outsource Underwriting Services

Why MCA Businesses Need Outsourcing — Cut Costs by 60%

January 31, 2025

Quick Answer

Why should services/ target=_blank rel=noopener noreferrer>ourcing-guide/ target=_blank rel=noopener noreferrer>mca-underwriting-complete-guide/ target=_blank rel=noopener noreferrer>MCA companies outsource underwriting? MCA companies should outsource underwriting for cost savings, expertise, focus, scalability, and speed – the five reasons to outsource MCA underwriting that every funder should evaluate: cost savings of 40 to 60 percent compared to in-house teams, access to specialized MCA underwriting expertise without hiring overhead, the ability to focus internal resources on core business activities like deal origination and merchant relationships, instant scalability from 10 to 1,000 deals per month, and 24-hour turnaround with 99 percent accuracy. The US merchant cash advance market is projected to grow from $19.7 billion to over $32 billion by 2032, making operational efficiency through outsourcing a competitive necessity rather than an option [R1].

Key Takeaways:

- MCA companies save 40-60% on underwriting costs by outsourcing to specialized BPO partners

- In-house underwriters cost $65,000-$85,000/yr each; outsourced equivalent costs 40-60% less with zero hiring overhead

- Specialized MCA outsourcing firms use HeronData, Ocrolus, and MoneyThumb for more accurate financial analysis

- Outsourcing allows MCA funders to scale from 10 to 1,000+ deals per month without infrastructure investment

- Leading MCA outsourcers deliver 24-hour turnaround with 99% accuracy versus 3-5 days in-house

1. Slash Operational Costs – Save 40-60% on Underwriting

Cost reduction is the most immediate and measurable reason. Understanding outsource MCA underwriting cost vs in-house cost is the first step in the evaluation MCA companies choose to outsource underwriting. The numbers are straightforward. MCA company cost savings from outsourcing range from 40 to 60 percent depending on volume and service scope.

The True Cost of In-House MCA Underwriting

A single in-house MCA underwriter costs between $65,000 and $85,000 per year in salary alone. Add benefits at 25 to 30 percent, training costs, software licenses for document processing tools, and management overhead, and the true annual cost per underwriter exceeds $100,000. For a team of three to five underwriters, that is $300,000 to $500,000 per year in operational costs before a single deal is priced [R2].

Hidden costs make the picture worse. Underwriter turnover in the MCA industry is high – experienced underwriters are in constant demand, and replacing one costs 30 to 50 percent of their annual salary in recruiting, onboarding, and ramp-up time. New underwriters take three to six months to reach full productivity, meaning every hire carries a significant productivity loss during the learning period.

Cost Comparison: In-House vs Outsourced

Beyond Direct Salary – The Hidden Savings

Outsourcing eliminates the entire HR overhead of the underwriting function. No job postings, no interview cycles, no benefits administration, no payroll processing, no severance payments. When deal volume drops, you scale down without layoffs. When volume spikes, you scale up without frantic hiring. This flexibility is invisible on a cost comparison spreadsheet but becomes the single most valuable financial benefit when market conditions shift. Scaling MCA operations through outsourcing removes the fixed-cost anchor that keeps growing funders from expanding profitably.

For MCA funders evaluating whether to outsource MCA underwriting services. MCA underwriting services from specialized partners deliver better accuracy at lower cost, the cost analysis is not close. The best MCA outsourcing companies deliver equivalent or better quality at 40 to 60 percent less than in-house operations.

Related: Loan Underwriting Process: Complete Guide for Lenders (2026) | Merchant Cash Advance: The Complete Guide for Borrowers and Lenders (2026) | MCA Underwriting: The Complete Guide to Merchant Cash Advance Underwriting Process

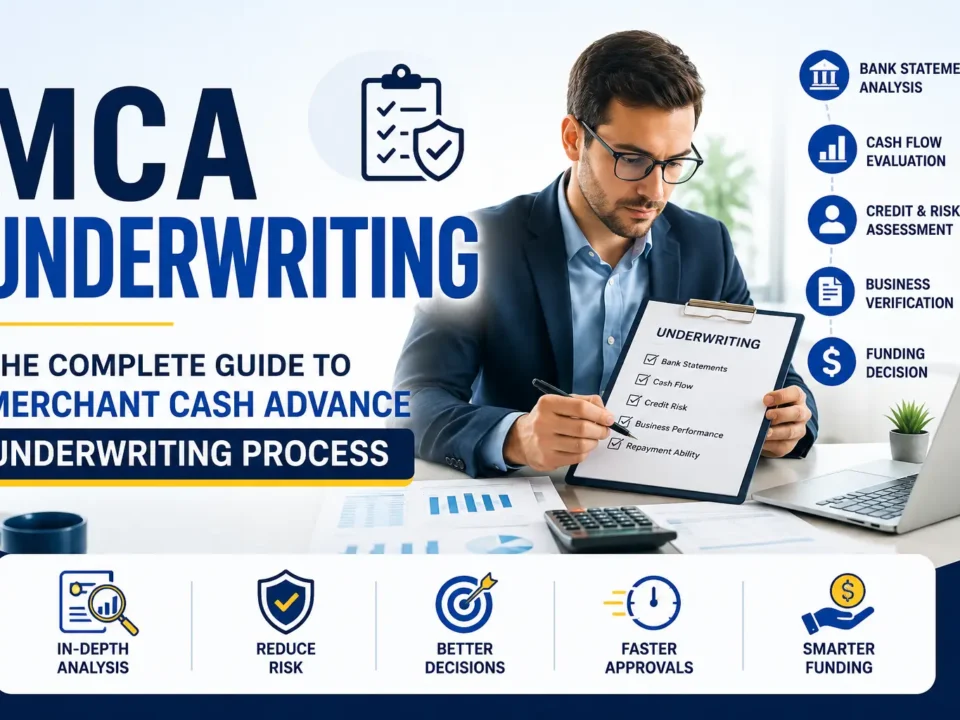

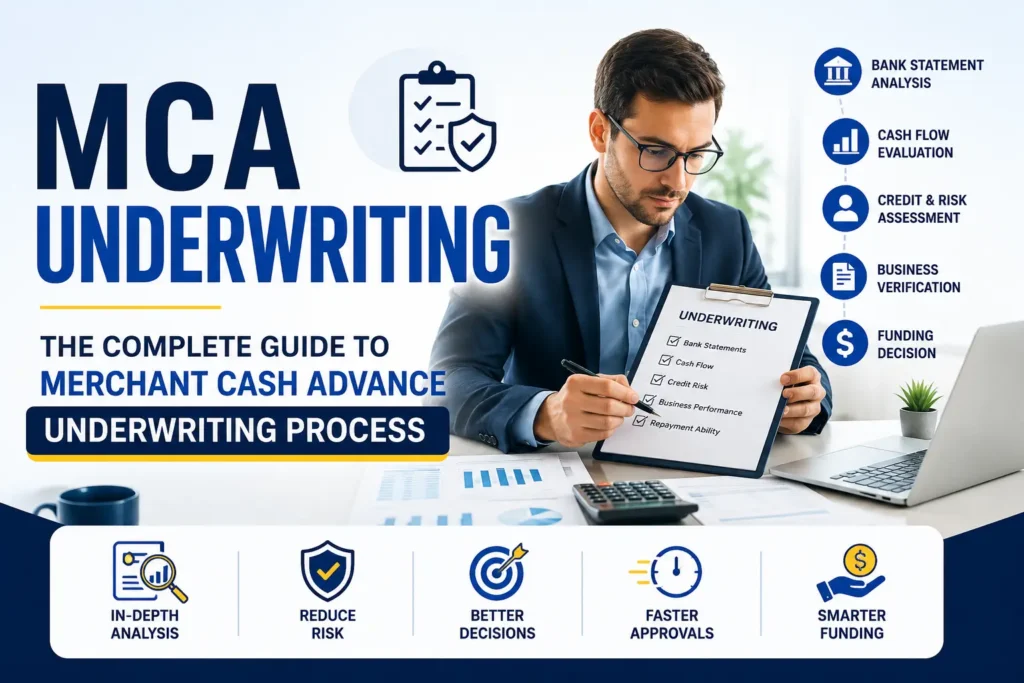

2. Access to Specialized MCA Underwriting Expertise

Underwriting in the merchant cash advance space requires specific knowledge that general underwriting experience does not provide. Outsourcing gives MCA companies immediate access to teams with this specialized expertise.

The MCA Knowledge Gap

New in-house underwriters typically take three to six months to ramp up on MCA-specific requirements. They need to learn the nuances of daily repayment cycles, factor rate calculations based on risk profiles, NSF pattern analysis, bank statement scrubbing protocols, and the regulatory landscape that governs alternative lending.

During this ramp period, underwriting quality suffers. Errors in risk assessment lead to either overpriced deals that merchants reject or underpriced deals that increase default rates. Every underwriting mistake during the learning phase costs real money – and the company bears the full cost of these errors.

Tool and Technology Ecosystem

Experienced MCA outsourcing firms bring proficiency with the industry-standard tools that enable fast, accurate underwriting. HeronData, Ocrolus, and MoneyThumb are the primary platforms for bank statement analysis and financial document processing [R3]. Decision Logic and Plaid handle data verification and financial aggregation. On the CRM side, Salesforce, HubSpot, LendSaas, and MCA Pilot are the platforms that specialized MCA underwriters use daily.

An in-house team would need to invest significant time and money to achieve the same tool proficiency that an outsourced team already has on day one.

Accuracy Improvements

In-house underwriting teams typically achieve 85 to 90 percent accuracy on standard files. The best MCA outsourcing companies consistently deliver 99 percent accuracy – a direct result of specialized training, daily volume, and dedicated quality control processes. For a funder processing 200 deals per month, a 10 percent accuracy gap means 20 deals per month with incorrect risk assessments. The financial impact of those errors far outweighs any cost savings from keeping underwriting in-house.

3. Free Your Team to Focus on Growth and Deal Origination

Underwriting consumes operational hours that could be spent on revenue-generating activities. This is the opportunity cost argument for outsourcing – and for growing MCA companies, it is often the most persuasive reason.

Underwriting as a Bottleneck

At most MCA companies, underwriting consumes 60 percent or more of total operational hours. Every hour an internal team member spends on bank statement analysis, risk scoring, or stipulation clearing is an hour they are not spending on deal origination, merchant relationships, or portfolio management.

The bottleneck effect is real. When underwriting slows down, the entire deal pipeline stalls. Deals take longer to fund, merchants lose patience and shop competitors, and the company’s reputation for speed erodes. For MCA funders who win deals based on speed of funding, an underwriting bottleneck is a direct competitive disadvantage.

What Top Performers Do Differently

The highest-performing MCA funders outsource 80 percent or more of their back-office operations. MCA back office support covers everything from document processing to compliance reporting. Their internal teams focus exclusively on three functions: merchant relationship management, deal sourcing and origination, and strategic growth planning. Underwriting, document processing, CRM management, and compliance monitoring are handled by specialized BPO partners who do those tasks at higher quality and lower cost [R4].

Real Impact

One MCA funder who outsourced full-cycle underwriting to a specialized partner achieved three times the deal volume with the same internal headcount. The internal team shifted from processing paperwork to building merchant relationships and sourcing new deals. Within six months, the company’s funding volume increased by 180 percent without adding a single internal employee.

4. Scale Instantly Without Hiring Headaches

Scalability is the reason that separates MCA outsourcing from a nice-to-have to a strategic necessity. The ability to add or reduce underwriting capacity in days rather than months gives MCA companies a competitive advantage that in-house operations cannot match.

The Hiring Problem

Hiring an in-house MCA underwriter takes four to eight weeks for recruitment, plus three to six months to reach full productivity. For a company experiencing seasonal spikes or entering a growth phase, this timeline is disastrous. By the time the new underwriter is productive, the spike has passed or the competition has captured the market share.

How BPO Partners Enable True Scalability

A good MCA outsourcing partner can add 50 deals of monthly capacity in 48 hours. No interviews, no training, no desk setup. The partner simply assigns additional pre-trained underwriters who are already proficient with HeronData, Ocrolus, and your CRM platform. When volume normalizes, you scale back down without the pain of layoffs.

This flexibility is enabled by per-deal pricing models. You pay only for what you use. A month with 50 deals costs half of a month with 100 deals. Compare that to in-house operations, where fixed salary costs remain the same regardless of deal volume.

From Startup to Enterprise Without Growing Pains

MCA funders who start with an outsourcing partner can scale from 10 deals per month to 1,000 without changing their operational model. The same partner, the same processes, the same quality standards – just more capacity. This is impossible with in-house teams, which require continuous hiring, training, and management overhead at every growth milestone.

5. Get 24-Hour Turnaround with 99% Accuracy

Speed is the defining competitive advantage in MCA funding. The faster a deal funds, the more deals a company closes. Outsourcing delivers speed that in-house operations struggle to match.

The Speed Advantage

In-house underwriting teams typically take three to five business days to complete a standard underwriting file. Outsourced MCA underwriting teams working across timezones deliver a 24-hour turnaround on the same files. For a merchant who needs funding this week, the difference between a one-day and five-day turnaround is the difference between closing the deal and losing it.

Accuracy at Speed – The Automation and Human Balance

The best MCA outsourcing companies achieve speed without sacrificing accuracy by combining automated tools with human quality review. Automated platforms like HeronData and Ocrolus. MCA automation tools enable speed and accuracy that manual processes cannot match like Ocrolus and HeronData extract structured data from bank statements in minutes. Experienced underwriters then review the data, apply risk models, and make funding recommendations. The result is 24-hour turnaround with 99 percent accuracy – a combination that in-house teams cannot match because they lack both the volume to justify the automation investment and the specialized training to maintain quality at speed [R5].

How Speed Translates to Revenue

Every day saved in the underwriting cycle increases deal closure rates. MCA funders who offer same-week funding capture a disproportionate share of high-quality merchants who need capital quickly. For a funder processing 100 deals per month, reducing underwriting time from five days to one day enables three times the deal throughput without any increase in deal flow. The revenue impact is immediate and compounding.

MCA Underwriting: In-House vs Outsourcing ROI

| Factor | In-House | Outsourced | Annual Impact for 200 files/month |

|---|---|---|---|

| Staffing cost | $120K-$160K (2 underwriters) | $60K-$90K | Save $60K-$70K |

| Processing time | 48-72 hours | 12-24 hours | Faster funding, better broker relationships |

| Capacity ceiling | 60-80 files/month per team | 100-200+ files/month | 100%+ growth without hiring |

| Quality/accuracy | 97-98% | 97-98% | Comparable with lower cost |

| Recovery from turnover | 4-8 weeks hiring gap | Instant replacement | Zero downtime |

| Total annual savings | – | – | $70K-$100K+ |

Challenge: An MCA company funding $50M+ monthly was processing 200+ deals per week with an in-house underwriting team of 8. Turnaround time was 6-8 hours per deal, costing them quality submissions. In-house cost per underwrite was $38, and night shifts were understaffed.

Solution: Procizo deployed 6 dedicated underwriters across US time zones, handling bank statement scrubbing, paper grading, stacking detection, and pre-funding quality checks inside the client’s platform via secure VPN.

Results (6 months):

- Turnaround: 6-8 hrs ? 90 min (75% faster)

- Cost per underwrite: $38 ? $14 (63% savings)

- Weekly deal capacity: 200 ? 450+

- Same-day funding rate: 45% ? 88%

- Stacking detection accuracy: 97%

Frequently Asked Questions

Why outsource MCA underwriting?

MCA companies outsource underwriting to reduce costs by 40-60%, access specialized expertise, focus on core business activities, scale instantly without hiring overhead, and achieve 24-hour turnaround with 99 percent accuracy.

What are the benefits of MCA outsourcing?

The main benefits are cost savings, immediate access to experienced MCA underwriters proficient in HeronData, Ocrolus, and MoneyThumb, flexible scalability from 10 to 1,000 deals per month, faster funding cycles, and reduced operational risk through SOC 2 compliant processes.

How much can MCA companies save by outsourcing?

MCA companies typically save 40 to 60 percent on underwriting costs compared to in-house operations. A funder spending $300,000 to $500,000 per year on an in-house team can expect to pay $120,000 to $250,000 for equivalent outsourced services with faster turnaround and higher accuracy.

Is MCA underwriting outsourcing reliable?

Yes, when you work with experienced, SOC 2 certified partners. The best MCA outsourcing firms achieve 99 percent accuracy and 24-hour turnaround on standard files, with documented quality control processes and client references.

How fast is outsourced MCA underwriting?

Outsourced MCA underwriting typically delivers 24-hour turnaround on standard files, compared to three to five business days for in-house teams.

What tools do MCA outsourcers use?

The most common tools are HeronData, Ocrolus, MoneyThumb, and Decision Logic for bank statement analysis; Salesforce, HubSpot, Zoho, and LendSaas for CRM; and Plaid for financial data aggregation.

Ready to Cut Your Underwriting Costs by 40-60%?

Procizo specializes in MCA underwriting outsourcing for US lenders, brokers, and funders. Our teams deliver 24-hour turnaround, 99 percent accuracy, and flexible pricing that scales with your deal volume. Get in touch for a free cost comparison and pilot program.

Beyond the 5 Reasons – Additional Benefits Worth Considering

While the five reasons above cover the primary motivations for outsourcing, MCA companies also benefit from several secondary advantages that compound over time.

Reduced Technology Investment

Every in-house underwriting team needs document processing tools, CRM licenses, data verification software, and compliance monitoring platforms. The combined cost of software licenses for a five-person underwriting team ranges from $15,000 to $40,000 per year. Outsourced partners include all technology costs in their pricing, eliminating this capital expenditure.

Compliance Risk Mitigation

The MCA regulatory environment has become significantly more demanding. CFPB Section 1071 compliance requirements, state-level disclosure laws in Missouri, Connecticut, Texas, and Virginia, and increasing scrutiny from regulators create an environment where compliance mistakes are expensive. SOC 2 certified outsourcing partners maintain audit-ready documentation for every deal, reducing regulatory risk for their clients [R6]. This compliance infrastructure is expensive to build in-house but comes standard with a qualified BPO partner.

Access to Continuous Improvement

Specialized MCA outsourcing firms process thousands of deals per month across multiple clients. This volume gives them data and insights that no single in-house team can match. They continuously refine their processes, update their risk models, and adopt new tools based on what works across their entire client base. In-house teams, limited to their own deal volume, cannot match this rate of improvement.

How to Take Action – Your Next Steps

If the five reasons above resonate with your situation, here is a practical action plan:

- Run the numbers – Calculate your true per-deal underwriting cost including all salaries, benefits, software, and overhead

- Compare against outsourced pricing – Request proposals from two to three MCA-specialized BPO partners

- Start with a pilot – Run 10 to 20 deals through an outsourced partner to validate quality and turnaround

- Evaluate the results – Compare accuracy, speed, and cost against your in-house baseline

- Scale gradually – Start with one function (underwriting or bank statement scrubbing) and expand as trust builds

Most MCA funders who follow this process never return to in-house underwriting. The cost savings, speed, and quality improvements are too substantial to ignore.

References

| Code | Source | Link |

|---|---|---|

| [R1] | IBISWorld – Industry Research & Market Data | View ? |

| [R2] | Dun & Bradstreet – Industry Research & Market Data | View ? |

| [R3] | Experian – Industry Research & Market Data | View ? |

| [R4] | Federal Reserve – Industry Research & Market Data | View ? |

| [R5] | SBA – Industry Research & Market Data | View ? |

| [R6] | Procizo Outsourcing LLC – Loan Underwriting Process: Complete Guide for Lenders (2026) | View ? |

| [R7] | Procizo Outsourcing LLC – Merchant Cash Advance: The Complete Guide for Borrowers and Lenders (2026) | View ? |

| [R8] | Procizo Outsourcing LLC – MCA Underwriting: The Complete Guide to Merchant Cash Advance Underwriting Process | View ? |

| [R9] | Procizo Outsourcing LLC – What Is MCA Underwriting? The Complete Process for Funders (2026) | View ? |

| [R10] | Procizo Outsourcing LLC – What Is Underwriting? Complete Guide for Business Lending (2026) | View ? |

| [R11] | Procizo Outsourcing LLC – The Complete Guide to MCA Underwriting Outsourcing (2026) | View ? |

Ready to Streamline Your Mca Underwriting Support?

Procizo Outsourcing LLC provides end-to-end MCA underwriting support with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement – no long-term commitment required.

No commitment required . 2-3 week onboarding . SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

Ready to Streamline Your Mca Underwriting Support?

Procizo Outsourcing LLC provides end-to-end MCA underwriting support with transparent pricing, dedicated teams, and rapid onboarding. Start with a pilot engagement – no long-term commitment required.

No commitment required . 2-3 week onboarding . SOC 2 Type II security

Editorial Oversight: Content reviewed and approved by the Procizo Outsourcing LLC team based on internal research, operational experience, industry reports, and publicly available data.

Research Methodology: This content was created using a combination of Procizo Outsourcing LLC’s operational expertise, industry publications, academic research, government resources, and verified third-party sources.

{kind=link}

{kind=link}